Stop Bleeding Rent: How Smart Market Slashes Vacancy Costs

Stop Bleeding Rent: How Smart Market Timing Slashes Vacancy Costs

Rental market timing is the practice of aligning listing, leasing, and renewal activities with periods of high renter demand and low competing supply. For landlords managing 1 to 100 units, even shaving one week off a vacancy period can recover more income than a modest annual rent increase. A unit renting at $1,650 per month with $300 in monthly operating expenses costs approximately $65 per day when vacant. One poorly timed 20-day gap erases more than a 3% annual rent bump before a single improvement is made to the property.

Most landlords lose this money not from bad management but from bad timing. A lease that ends in January creates a vacancy during the slowest leasing month of the year. The same unit, with a lease engineered to expire in July, fills in days rather than weeks. The calendar is the lever, and most landlords are not using it.

Why Market Timing Matters More Than Most Landlords Realize

Renter search traffic and applications peak nationally in late May and June. Winter months from December through February are the slowest leasing period of the year, with more concessions and longer days on market. Regional patterns vary: Sun Belt metros with high new supply tend to show flatter seasonal premiums, while Midwestern cities retain stronger summer rent lifts.

Asset type also matters. Single-family homes attract families who prefer summer moves aligned with school calendars. Urban studios lease faster in spring. Hyper-local signals including university calendars, employer hiring cycles, and neighborhood events can create demand windows that do not show up in national data.

Tracking your own days-on-market history by unit and season is the most accurate way to identify the demand windows that apply to your specific portfolio.

Four Levers That Put Timing in Your Control

Lease-term engineering is the most underused tool in a small landlord's toolkit. The standard 12-month lease defaults to whatever expiration date the first signing happened to produce. Offering 9-, 10-, 13-, or 15-month terms at lease signing or renewal gives landlords a mechanism to gradually realign expirations with peak demand months without forcing tenants into uncomfortable ultimatums. A framing like "10-month term at current rent or 12 months at a $15 increase" gives tenants a real choice while moving the landlord toward a better expiration window.

Renewal negotiation windows should open 90 days before lease end at minimum, and earlier for leases expiring in winter. Starting the conversation late leaves no room to adjust terms, address tenant concerns, or pivot to marketing if renewal is unlikely. Sharing local data on seasonal demand during the renewal conversation, such as the fact that June rents average slightly higher and fill faster, gives tenants context for a term adjustment rather than making it feel arbitrary.

Dynamic pricing windows require a willingness to price slightly below market in off-peak months to avoid prolonged vacancy, and to aim for the upper quartile of comparable units during peak months. A small rent premium in June or July disappears entirely if the unit sits idle for five extra days while trying to capture it. A useful signal: more than eight showings without an application typically indicates the unit is overpriced for current demand.

Flexible move-in dates and targeted concessions close the gap between what the market offers and what your calendar requires. Advertising availability up to 30 days before a unit vacates captures prospective tenants who are planning ahead. In slow months, a one-time $200 concession often costs less than 10 vacant days at $65 per day. Prorated partial months allow move-in dates to align with peak demand without requiring tenants to double up on rent.

The Numbers Behind One Smart Term Decision

Consider a one-bedroom unit in a mid-sized city renting at $1,800 per month with $300 in monthly operating expenses. Daily vacancy cost is approximately $70.

A lease that ends January 31 and re-leases February 15 produces 15 vacant days at $70, or $1,050 in losses.

The same unit, with an 11-month term offered the prior year to shift the expiration to July 31, re-leases in 3 days. Vacancy cost: $210.

Savings from one term adjustment: $840, roughly half a month's rent. Across four units over five years, that difference compounds to approximately $17,000 in preserved net operating income.

The math is not complicated. The discipline is in applying it consistently rather than defaulting to 12-month terms out of habit.

Common Timing Mistakes That Cost Landlords Money

Chasing top-of-market rent in off-season months is one of the most expensive timing errors a landlord can make. Being 2% overpriced in January can add weeks of vacancy that no future rent increase will recover.

Allowing leases to auto-renew month-to-month eliminates control over expiration timing entirely and almost guarantees future winter vacancies.

Overlapping turnovers across multiple units in the same portfolio double cash-flow strain and stretch vendor availability, extending the vacant period for each unit.

Ignoring regional supply pipelines means missing the signal that new construction is about to increase competition in your submarket, which shifts the pricing and timing calculus for that leasing season.

How Shuk Supports Market Timing

Shuk's Lease Indication Tool polls tenants monthly beginning six months before lease end, giving landlords early renewal signals at the 120-, 90-, and 60-day marks. That visibility allows landlords to begin renewal conversations or marketing preparation well before tenants start shopping elsewhere, with enough runway to adjust term lengths and pricing before the window closes.

Year-round listing visibility on Shuk keeps properties discoverable even when occupied, showing upcoming availability to prospective tenants who are planning ahead. Landlords who maintain continuous listings build a warm pipeline between leases rather than restarting from zero at every turnover.

Frequently Asked Questions

What is rental market timing and why does it matter for landlords?

Rental market timing is the practice of aligning listing, leasing, and renewal activities with periods of high renter demand and low supply. Renter search activity peaks nationally in late May and June and drops significantly from December through February. A unit that vacates in winter takes longer to fill and often requires concessions. Aligning lease expirations with peak demand months is one of the highest-return adjustments a self-managing landlord can make.

How much does poor lease timing actually cost?

Daily vacancy cost equals monthly rent plus operating expenses divided by 30. For a unit at $1,800 rent with $300 in monthly expenses, that is $70 per day. A lease that ends in January and takes 15 days to fill costs $1,050 in vacancy losses. The same unit with an expiration timed to July, filling in 3 days, costs $210. The difference from one term adjustment is $840. Across multiple units over several years, timing gaps compound into significant lost income.

What lease terms help avoid off-season vacancies?

Offering 9-, 10-, 13-, or 15-month lease terms at signing or renewal allows landlords to gradually realign expirations with peak demand months without requiring large rent adjustments. The key is framing the option as a choice rather than a requirement. For multi-unit portfolios, staggering expirations across different months also prevents overlapping turnovers that strain cash flow and vendor availability simultaneously.

When should a landlord start a renewal conversation?

Renewal conversations should begin at least 90 days before lease end, and earlier for leases expiring in winter when demand is lowest. Starting late leaves no time to adjust terms, address tenant concerns, or prepare marketing if the tenant plans to leave. For winter expirations, beginning outreach 120 days in advance gives enough runway to offer a term adjustment that shifts the next expiration into a more favorable leasing season.

Is it better to offer a concession or hold firm on rent during slow leasing months?

In most cases, a targeted one-time concession costs less than extended vacancy. For a unit generating $70 per day in vacancy costs, a $200 move-in concession breaks even at fewer than three vacant days. Holding firm on rent during off-peak months while the unit sits empty for an additional week or two typically produces a larger financial loss than the concession amount. Price slightly below the upper quartile of comparable units during slow months and aim for premium pricing during peak demand periods.

Schedule a quick demo to receive a free trial and see how data-driven tools make rental management easier.

Stop Bleeding Rent: How Smart Market Timing Slashes Vacancy Costs

Rental market timing is the practice of aligning listing, leasing, and renewal activities with periods of high renter demand and low competing supply. For landlords managing 1 to 100 units, even shaving one week off a vacancy period can recover more income than a modest annual rent increase. A unit renting at $1,650 per month with $300 in monthly operating expenses costs approximately $65 per day when vacant. One poorly timed 20-day gap erases more than a 3% annual rent bump before a single improvement is made to the property.

Most landlords lose this money not from bad management but from bad timing. A lease that ends in January creates a vacancy during the slowest leasing month of the year. The same unit, with a lease engineered to expire in July, fills in days rather than weeks. The calendar is the lever, and most landlords are not using it.

Why Market Timing Matters More Than Most Landlords Realize

Renter search traffic and applications peak nationally in late May and June. Winter months from December through February are the slowest leasing period of the year, with more concessions and longer days on market. Regional patterns vary: Sun Belt metros with high new supply tend to show flatter seasonal premiums, while Midwestern cities retain stronger summer rent lifts.

Asset type also matters. Single-family homes attract families who prefer summer moves aligned with school calendars. Urban studios lease faster in spring. Hyper-local signals including university calendars, employer hiring cycles, and neighborhood events can create demand windows that do not show up in national data.

Tracking your own days-on-market history by unit and season is the most accurate way to identify the demand windows that apply to your specific portfolio.

Four Levers That Put Timing in Your Control

Lease-term engineering is the most underused tool in a small landlord's toolkit. The standard 12-month lease defaults to whatever expiration date the first signing happened to produce. Offering 9-, 10-, 13-, or 15-month terms at lease signing or renewal gives landlords a mechanism to gradually realign expirations with peak demand months without forcing tenants into uncomfortable ultimatums. A framing like "10-month term at current rent or 12 months at a $15 increase" gives tenants a real choice while moving the landlord toward a better expiration window.

Renewal negotiation windows should open 90 days before lease end at minimum, and earlier for leases expiring in winter. Starting the conversation late leaves no room to adjust terms, address tenant concerns, or pivot to marketing if renewal is unlikely. Sharing local data on seasonal demand during the renewal conversation, such as the fact that June rents average slightly higher and fill faster, gives tenants context for a term adjustment rather than making it feel arbitrary.

Dynamic pricing windows require a willingness to price slightly below market in off-peak months to avoid prolonged vacancy, and to aim for the upper quartile of comparable units during peak months. A small rent premium in June or July disappears entirely if the unit sits idle for five extra days while trying to capture it. A useful signal: more than eight showings without an application typically indicates the unit is overpriced for current demand.

Flexible move-in dates and targeted concessions close the gap between what the market offers and what your calendar requires. Advertising availability up to 30 days before a unit vacates captures prospective tenants who are planning ahead. In slow months, a one-time $200 concession often costs less than 10 vacant days at $65 per day. Prorated partial months allow move-in dates to align with peak demand without requiring tenants to double up on rent.

The Numbers Behind One Smart Term Decision

Consider a one-bedroom unit in a mid-sized city renting at $1,800 per month with $300 in monthly operating expenses. Daily vacancy cost is approximately $70.

A lease that ends January 31 and re-leases February 15 produces 15 vacant days at $70, or $1,050 in losses.

The same unit, with an 11-month term offered the prior year to shift the expiration to July 31, re-leases in 3 days. Vacancy cost: $210.

Savings from one term adjustment: $840, roughly half a month's rent. Across four units over five years, that difference compounds to approximately $17,000 in preserved net operating income.

The math is not complicated. The discipline is in applying it consistently rather than defaulting to 12-month terms out of habit.

Common Timing Mistakes That Cost Landlords Money

Chasing top-of-market rent in off-season months is one of the most expensive timing errors a landlord can make. Being 2% overpriced in January can add weeks of vacancy that no future rent increase will recover.

Allowing leases to auto-renew month-to-month eliminates control over expiration timing entirely and almost guarantees future winter vacancies.

Overlapping turnovers across multiple units in the same portfolio double cash-flow strain and stretch vendor availability, extending the vacant period for each unit.

Ignoring regional supply pipelines means missing the signal that new construction is about to increase competition in your submarket, which shifts the pricing and timing calculus for that leasing season.

How Shuk Supports Market Timing

Shuk's Lease Indication Tool polls tenants monthly beginning six months before lease end, giving landlords early renewal signals at the 120-, 90-, and 60-day marks. That visibility allows landlords to begin renewal conversations or marketing preparation well before tenants start shopping elsewhere, with enough runway to adjust term lengths and pricing before the window closes.

Year-round listing visibility on Shuk keeps properties discoverable even when occupied, showing upcoming availability to prospective tenants who are planning ahead. Landlords who maintain continuous listings build a warm pipeline between leases rather than restarting from zero at every turnover.

Frequently Asked Questions

What is rental market timing and why does it matter for landlords?

Rental market timing is the practice of aligning listing, leasing, and renewal activities with periods of high renter demand and low supply. Renter search activity peaks nationally in late May and June and drops significantly from December through February. A unit that vacates in winter takes longer to fill and often requires concessions. Aligning lease expirations with peak demand months is one of the highest-return adjustments a self-managing landlord can make.

How much does poor lease timing actually cost?

Daily vacancy cost equals monthly rent plus operating expenses divided by 30. For a unit at $1,800 rent with $300 in monthly expenses, that is $70 per day. A lease that ends in January and takes 15 days to fill costs $1,050 in vacancy losses. The same unit with an expiration timed to July, filling in 3 days, costs $210. The difference from one term adjustment is $840. Across multiple units over several years, timing gaps compound into significant lost income.

What lease terms help avoid off-season vacancies?

Offering 9-, 10-, 13-, or 15-month lease terms at signing or renewal allows landlords to gradually realign expirations with peak demand months without requiring large rent adjustments. The key is framing the option as a choice rather than a requirement. For multi-unit portfolios, staggering expirations across different months also prevents overlapping turnovers that strain cash flow and vendor availability simultaneously.

When should a landlord start a renewal conversation?

Renewal conversations should begin at least 90 days before lease end, and earlier for leases expiring in winter when demand is lowest. Starting late leaves no time to adjust terms, address tenant concerns, or prepare marketing if the tenant plans to leave. For winter expirations, beginning outreach 120 days in advance gives enough runway to offer a term adjustment that shifts the next expiration into a more favorable leasing season.

Is it better to offer a concession or hold firm on rent during slow leasing months?

In most cases, a targeted one-time concession costs less than extended vacancy. For a unit generating $70 per day in vacancy costs, a $200 move-in concession breaks even at fewer than three vacant days. Holding firm on rent during off-peak months while the unit sits empty for an additional week or two typically produces a larger financial loss than the concession amount. Price slightly below the upper quartile of comparable units during slow months and aim for premium pricing during peak demand periods.

Schedule a quick demo to receive a free trial and see how data-driven tools make rental management easier.

{

"@context": "https://schema.org",

"@type": "FAQPage",

"mainEntity": [

{

"@type": "Question",

"name": "What is rental market timing and why does it matter for landlords?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Rental market timing is the practice of aligning listing, leasing, and renewal activities with periods of high renter demand and low supply. Renter search activity peaks nationally in late May and June and drops significantly from December through February. A unit that vacates in winter takes longer to fill and often requires concessions. Aligning lease expirations with peak demand months is one of the highest-return adjustments a self-managing landlord can make."

}

},

{

"@type": "Question",

"name": "How much does poor lease timing actually cost?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Daily vacancy cost equals monthly rent plus operating expenses divided by 30. For a unit at $1,800 rent with $300 in monthly expenses, that is $70 per day. A lease that ends in January and takes 15 days to fill costs $1,050 in vacancy losses. The same unit with an expiration timed to July, filling in 3 days, costs $210. The difference from one term adjustment is $840. Across multiple units over several years, timing gaps compound into significant lost income."

}

},

{

"@type": "Question",

"name": "What lease terms help avoid off-season vacancies?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Offering 9-, 10-, 13-, or 15-month lease terms at signing or renewal allows landlords to gradually realign expirations with peak demand months without requiring large rent adjustments. The key is framing the option as a choice rather than a requirement. For multi-unit portfolios, staggering expirations across different months also prevents overlapping turnovers that strain cash flow and vendor availability simultaneously."

}

},

{

"@type": "Question",

"name": "When should a landlord start a renewal conversation?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Renewal conversations should begin at least 90 days before lease end, and earlier for leases expiring in winter when demand is lowest. Starting late leaves no time to adjust terms, address tenant concerns, or prepare marketing if the tenant plans to leave. For winter expirations, beginning outreach 120 days in advance gives enough runway to offer a term adjustment that shifts the next expiration into a more favorable leasing season."

}

},

{

"@type": "Question",

"name": "Is it better to offer a concession or hold firm on rent during slow leasing months?",

"acceptedAnswer": {

"@type": "Answer",

"text": "In most cases, a targeted one-time concession costs less than extended vacancy. For a unit generating $70 per day in vacancy costs, a $200 move-in concession breaks even at fewer than three vacant days. Holding firm on rent during off-peak months while the unit sits empty for an additional week or two typically produces a larger financial loss than the concession amount. Price slightly below the upper quartile of comparable units during slow months and aim for premium pricing during peak demand periods."

}

}

]

}

Shuk helps landlords and property managers get ahead of vacancies, improve renewal visibility, and bring more predictability to every lease cycle.

Book a demo to get started with a free trial.

RentRedi Alternative: A Decision Guide for Landlords and Small Property Managers

If you are searching for a RentRedi alternative, you have likely hit a familiar friction point: the platform still works, but the workaround list keeps growing. Rent collection happens, but deposits and fees need manual cleanup. Maintenance requests come in, but tracking vendor status and recurring issues feels scattered. You can produce a basic report, but month-end close still means exporting to spreadsheets, reconciling in a separate accounting tool, or asking your CPA to make sense of the numbers.

This is the quiet tax of outgrowing entry-level property management software: not a single catastrophic failure, but constant friction. That friction shows up as missed follow-ups, slower owner updates, inconsistently applied late fees, and financial records that do not match your bank. Over time it affects tenant experience and renewals because tenants increasingly expect online-first service. Industry research found that 95% of rental owners are comfortable doing business online, up notably year over year, meaning digital workflows are now a baseline expectation rather than a differentiator.

The upside is that switching software is more common than it used to be and the return on investment can be real. Research on small landlord operations suggests meaningful annual savings through automation, with reported ROI of 300% to 500% within the first year when automation genuinely replaces manual work. This guide gives you a structured seven-step framework to decide whether to stay put, upgrade your process, or move to the RentRedi replacement that fits your portfolio.

What to Compare and Why It Matters More Than Price

Alternatives to RentRedi span a wide range: some tools are landlord-first and lightweight, others are designed for property managers with complex accounting and compliance requirements. The mistake most operators make is comparing only the subscription price, or worse, comparing feature checklists without testing how those features work in real conditions like applying partial payments, handling chargebacks, or reconciling deposits.

A more useful approach is to evaluate software through the lens of your operating model.

Cash-flow accuracy: How confidently can you answer what you actually collected and what is still owed without spreadsheet work?

Maintenance workflows: Are requests trackable end to end from triage through assignment, vendor communication, invoice, and resident update?

Scalability: Will the system still feel clean at 50 doors, 150 doors, or 300?

Integrations: Can it connect to your bookkeeping, bank feeds, listing channels, and reporting tools, or do you re-enter data across systems?

Support: When rent is missing, you do not want a forum thread. You want a resolution path and clear accountability.

The market is moving quickly. The global property management software market was valued at $24.18 billion in 2024 and is projected to reach $52.21 billion by 2032, driven by cloud adoption and automation. More platforms and more features mean more reasons to be intentional about your stack rather than defaulting to whatever is cheapest.

Seven Steps to Choose the Best RentRedi Alternative

Step 1. Define Your Must-Win Outcomes Before Looking at Features

Before evaluating any property management software, define what better must mean for your business. Features are only valuable if they improve measurable outcomes.

Start with three buckets. Time savings: what tasks are consuming your week, whether that is leasing coordination, payment follow-up, maintenance coordination, or owner reporting? Financial accuracy: are you reconciling monthly and are you confident in your delinquency reporting? Tenant experience: tenants increasingly choose rentals based on the service experience, particularly tech-enabled convenience around payments, communication, and maintenance.

Write down five KPIs you want software to improve before you begin any demos. Examples might be closing books by the fifth of each month, reducing late rent follow-ups, or getting maintenance first responses under four hours. Use those KPIs as your scoring criteria rather than marketing claims.

Mini case study: Maria owns 15 units across two small buildings. Rent collection works, but month-end is consistently chaotic: she exports transactions, tags them in spreadsheets, and her CPA still finds mismatches at tax time. Maria's must-win outcome is not a new tenant portal. It is clean monthly books and a faster close process.

Step 2. Compare Rent Collection as a Cash-Flow System, Not a Payment Button

Rent collection is where small workflow gaps become significant cash-flow problems, especially when you scale beyond a handful of doors. When evaluating a RentRedi alternative, test the specific scenarios that expose platform weaknesses rather than the common case.

How does the ledger behave if a tenant pays half now and half later? Can you set late fee rules that reflect your actual lease terms including grace periods, caps, and one-time versus recurring charges? Are there options for ACH, debit, and credit, and do you control who pays the processing fees? Do payments post immediately or after settlement, and are pending versus completed amounts clearly distinguished? Does the platform automatically remind tenants of upcoming and overdue amounts, and can you log notices and document communications for compliance purposes?

Industry data suggests tenants who use online payment functions can be twice as likely to pay on time, which directly stabilizes cash flow. The best RentRedi alternative for your portfolio may simply be the tool that drives the highest tenant adoption of online payments with the least confusion.

Mini case study: Devin manages 80 units. He does not need sophisticated marketing tools. He needs fewer disputes over whether a payment was made. In every demo he asks vendors to show exactly where he would click to confirm payment status and how a reversed payment appears in the ledger. The platform that wins is the one that makes disputes rare and resolution fast.

During trials, run a mock rent cycle with at least three test scenarios covering on-time autopay, a late payer, and a partial payment. If you cannot simulate edge cases, you are making a purchasing decision without the information that matters most.

Step 3. Treat Screening, Leases, and Compliance as a Single Workflow Chain

Many landlords compare screening vendors and e-signature features in isolation. In practice, what matters is whether the system supports a consistent and defensible leasing process from first contact to signed lease.

Look for application pipeline visibility that shows where each applicant stands without manual tracking. Evaluate screening speed and audit trail quality, because digital screening that can shorten time-to-approve while maintaining consistency is directly tied to reducing vacancy loss. Confirm that the platform supports lease templates and standardized addenda so you are not emailing PDFs and tracking versions manually. Verify that the full chain from application through screening result through lease through notices is stored and retrievable for fair housing compliance or dispute documentation.

Example: A couple applying to Sam's duplex claims they were treated inconsistently compared to another applicant. Sam cannot prove his process because notes are scattered across texts and email threads. A stronger system would show time-stamped actions, consistent criteria, and stored communications that make the process reproducible and defensible.

Ask each vendor directly: show me what an audit trail looks like for an applicant from first inquiry to move-in.

Step 4. Evaluate Maintenance as Your Retention Engine

If rent collection is the cash-flow engine of your portfolio, maintenance is the retention engine. Industry reporting consistently emphasizes maintenance operations as a competitive advantage because it affects renewals, reviews, and operational cost control over time.

Evaluate intake: can tenants submit requests with photos, video, categories, and permission to enter? Evaluate triage: can you set rules distinguishing emergencies from routine requests and assign by property, unit type, or vendor specialty? Evaluate status tracking: does the tenant receive automatic updates, or does every response require a manual step from your team? Evaluate vendor coordination: can vendors receive assignments, message within the ticket, and upload invoices? Evaluate recurring maintenance: can you schedule preventive work like filter changes, inspections, and gutter cleaning?

Mini case study: Aisha manages 120 units and noticed renewals declining. Her internal review showed slow maintenance response was the most common complaint. After implementing a platform with clearer ticket status and automated tenant updates, her team reduced inbound status calls and improved response consistency across the portfolio.

Create a list of ten standard repairs you handle regularly, such as a leak, no heat, appliance issue, lockout, and pest complaint. In demos, require the software to demonstrate the full workflow for each from tenant request through vendor invoice through owner reporting. If the demo uses only the ideal case, push for the edge cases.

Step 5. Treat Accounting Complexity as the Most Common Outgrowing Trigger

Landlords often tolerate basic ledgers until something forces the issue: adding more properties and being unable to break out performance by asset, a CPA requesting cleaner books with fewer manual exports, or beginning to manage for others and needing owner statements and trust account discipline.

Property management accounting has specific requirements that general business accounting does not address. Security deposits must be tracked as liabilities rather than income, owner disbursements must be clearly separated, and reconciliation discipline is foundational to reliable reporting and compliance.

When assessing a RentRedi replacement on accounting capability, ask whether you can customize the chart of accounts or map it to your CPA's structure. Confirm whether bank reconciliation is supported within the platform or requires exporting to a separate tool. Verify that security deposits are tracked correctly as liabilities. Confirm whether professional owner statements are producible without manual Excel formatting. And if you maintain a separate bookkeeping system, confirm whether the integration is genuinely bidirectional or requires re-entry.

Example: Luis manages 40 units for family members and friends. He does not need enterprise-grade accounting, but he does need consistent monthly owner statements and a straightforward way to tag expenses by property. He selects a platform based on owner reporting clarity and reconciliation workflow rather than the lowest monthly subscription.

Bring your CPA into the evaluation before you make a final decision. Ask what reports they need each month, then test whether the platform produces those reports without manual manipulation.

Step 6. Compare Pricing Using Total Operating Cost, Not Subscription Cost

Software pricing for small landlords typically follows recognizable patterns: per unit per month, flat monthly tiers, or bundled service fees covering payments, screening, and listings. The trap is focusing exclusively on the base plan.

Build a complete cost view that includes subscription fees at your current and projected unit counts, transaction fees for payment processing and expedited deposits, add-on costs for additional users, e-signatures, maintenance modules, or advanced reporting, and an honest estimate of labor cost. A cheaper platform that requires six additional hours of admin work per week is not cheaper in any meaningful sense.

Mini case study: Priya has 22 units. She considered switching because her current platform's basic plan appeared affordable, but she was absorbing costs through payment-related fees and manual reporting time that did not appear in the subscription comparison. She built a one-page cost model across three scenarios: staying with her current setup and keeping manual reporting, staying and buying add-ons, and switching to a system with stronger accounting and reporting. The winning choice was not the cheapest plan. It was the plan that reduced admin time and produced cleaner books.

Build a one-page cost model with three rows covering software fees, payment and screening fees, and hours per week of admin work. Assign a conservative hourly value to your time and run the comparison honestly.

Step 7. Validate User Experience, Support, and Scalability Before You Commit

Switching tools is significantly less risky when you treat it as a controlled migration rather than flipping a switch. Problems tend to surface at peak stress moments: month-end close, renewal season, and maintenance emergencies.

Evaluate whether a non-technical team member could learn the platform in a day. Confirm whether role-based access allows you to restrict what vendors and assistants can see. Ask whether onboarding is documented and structured rather than ad hoc. Test support responsiveness across the channels you would actually use. Confirm that all key data including tenants, leases, ledger history, and maintenance records can be exported if you ever need to switch again.

A practical migration plan for a small to mid-size portfolio: choose a cutover date at the beginning of a month for simplicity, export all current data before canceling anything, reconcile your ledger before migration rather than carrying forward errors, run both systems in parallel for two to four weeks to verify rent posting and maintenance intake, and send tenants a clear communication explaining what is changing, when it takes effect, and where to pay and submit maintenance going forward.

Example: Ben manages 210 units. He does not migrate everything simultaneously. He pilots the new platform on 30 units for one full rent cycle, then rolls out in waves. The result is fewer payment questions, fewer support tickets, and a cleaner transition for tenants.

Do not start migration during your busiest operational period. Most operators prefer a calm month with limited lease expirations and a predictable maintenance load.

RentRedi Alternative Evaluation Scorecard

Use this to compare platforms consistently. Score each item 1 to 5 and add notes.

Business fit and outcomes: Estimated weekly admin time reduction in hours. Improvement to on-time payment rates through tenant adoption. Impact on month-end close speed and spreadsheet dependency. Support for current portfolio size. Support for projected growth over the next 24 months.

Rent collection and resident payments: Autopay, partial payments, and late fee rules work as expected. Payment status is clearly shown as pending, settled, or reversed. Fee controls are transparent between tenant-paid and landlord-paid. Delinquency tracking and automated reminders function correctly.

Leasing and screening workflow: Application pipeline view and status tracking available. Screening process is consistent and produces an auditable record. E-sign leases and standardized addenda are stored in the platform. Tenant communications are centralized with email and text logs.

Maintenance and vendors: Tenant requests support photos and permission-to-enter. Triage rules, assignment workflows, and status tracking are functional. Vendor messaging within tickets and invoice upload are supported. Recurring maintenance scheduling is available.

Accounting and reporting: Bank reconciliation is supported in-platform or through a clean integration. Security deposits are tracked as liabilities rather than income. Property-level reporting covering income, expenses, and delinquency is available. Owner statements are producible without manual formatting for third-party management.

Integrations, security, and support: Data export covers tenants, leases, ledger, and maintenance history. Role-based access for assistants and vendors is configurable. Support channels and response times meet your operational needs. Onboarding documentation and migration assistance are included.

Frequently Asked Questions

How much does it cost to switch to a RentRedi alternative?

Direct costs typically include new subscription fees and any implementation assistance if you choose onboarding support. Indirect costs are the staff time required to export and import data, clean up your ledger, and communicate the change to tenants. The break-even depends on how manual your current process is. If switching reduces admin work meaningfully, the costs of migration are typically recovered within the first few months of operation.

Will I lose transaction history or maintenance records during migration?

You should not, provided you export data before canceling anything and are deliberate about what you import versus archive. A practical approach is to import current tenant balances and active leases while keeping older maintenance history in an accessible archive file. Reconcile and clean your records before cutover rather than carrying forward errors into the new system.

Are property management platforms typically month-to-month or contract-based?

It varies by platform. Some offer monthly plans with no commitment; others encourage annual terms. The key is to confirm cancellation terms, data export options, and whether pricing changes with unit count before you commit. If you are uncertain, start with a pilot group of units and avoid long-term commitments until you have run at least one full rent cycle in the new system.

How long does onboarding take for a small to mid-size portfolio?

For a handful of units with clean data, onboarding can be completed over a weekend. For 50 to 300 units, plan for a phased rollout over several weeks: approximately one week for data export and ledger cleanup, one week for platform configuration and testing, then a rent-cycle pilot before full rollout. Selecting a calm period with limited lease activity and predictable maintenance reduces the operational risk of the transition significantly.

Ready to see how Shuk compares on rent collection, maintenance workflows, accounting clarity, and owner reporting for portfolios of 1 to 100 units? Book a demo and walk through the platform with your specific unit count and operating model in mind.

What Property Managers Actually Do (And What You Can Do Yourself)

Property management is the set of systems a landlord or hired professional uses to protect rental income, maintain property condition, and stay legally compliant. A full-service property manager handles nine core functions: marketing, leasing, tenant screening, rent collection, maintenance coordination, inspections, bookkeeping, legal compliance, and evictions. For landlords managing 1-100 units, understanding each function clarifies which tasks can be handled independently with the right tools and which carry enough risk to warrant professional support.

The hidden costs of managing rentals without structure are real. One vacant month can erase a year of careful budgeting. Tenant turnover averages around $3,872 per unit once lost rent, make-ready costs, marketing, and concessions are combined. An eviction, when legal fees, lost rent, and damages are factored in, typically runs $3,500-$10,000. The better starting question is not "What does a property manager do?" It is: which tasks create the most risk and time pressure for your properties, and which ones can you systematize?

Traditional property managers earn their fee by running repeatable systems: consistent marketing, standardized screening, tight rent collection, controlled maintenance workflows, documented inspections, clean bookkeeping, compliance guardrails, and legally correct evictions when necessary. Many of those systems are no longer exclusive to professionals. With modern rental management software and a few simple operating procedures, small landlords can self-manage more than they might expect, as long as they are honest about their time, temperament, and risk tolerance.

This guide breaks down each core function and shows what you can realistically handle yourself, what is worth outsourcing, and what to do next.

The Core Job of a Property Manager and the DIY Decision Framework

A property manager's job is to protect income, asset condition, and legal compliance while reducing owner workload.

A full-service property manager typically covers nine operational functions:

- Marketing and advertising

- Leasing and showings

- Tenant screening and selection

- Rent collection and arrears management

- Maintenance coordination and vendor control

- Inspections (move-in, routine, move-out)

- Bookkeeping and owner reporting

- Legal compliance and policy management

- Evictions and dispute escalation

Professional managers also track performance metrics like days-to-lease, collection rate, maintenance response time, and occupancy and turnover rates. That performance-oriented mindset is a significant part of the value: they do not just complete tasks, they run a measurable process.

The DIY vs. hire reality for small landlords (1-100 units)

You can self-manage successfully if:

- Your properties are near you, or you have reliable local support.

- You can respond to issues consistently.

- You are willing to document everything and follow fair, repeatable criteria.

You should strongly consider hiring or partial outsourcing if:

- You are remote, frequently unavailable, or emotionally reactive with tenants.

- You struggle with documentation, deadlines, or bookkeeping.

- Your local legal environment is strict and highly procedural.

Fees for traditional management commonly run 8-12% of monthly rent, plus leasing fees (often 50-100% of one month's rent), renewal fees, and sometimes maintenance markups. Those numbers matter because they create a direct comparison: if you can replicate most systems with software plus selective outsourcing (such as a leasing-only service, an accountant, and an eviction attorney), you may maintain control while lowering total cost.

The sections below break down each function with what it involves, difficulty and time, risk, DIY tools and systems, and a clear DIY vs. hire call.

For the complete self-management workflow covering all tasks, see the complete guide to self-managing rental properties.

Nine Property-Manager Functions You Can Demystify and Systematize

3.1 Marketing and Advertising (Keeping Vacancy from Quietly Eating Your Profit)

What it involves: Pricing, listing creation, photos and video, syndication to rental sites, lead tracking, and showing coordination. Managers also monitor days-to-lease because vacancy is a direct income leak.

Typical difficulty and time: Moderate difficulty; time spikes during turnover.

DifficultyTime per vacant unitBest DIY use caseMedium2-6 hours upfront + showing timeLocal landlord with flexible schedule

Risk if done poorly: Mispricing and slow response increase vacancy. Vacancy rates move with supply and demand cycles, so a "wait and see" approach can cost real money when markets soften.

DIY tools and systems:

- Listing templates covering features, pet policy, fees, and screening criteria

- Photo checklist with phone tripod and consistent lighting

- Lead tracker spreadsheet or CRM-style pipeline

- Auto-replies and pre-screen questions to reduce wasted showings

Actionable tip: Set a speed-to-lead standard: respond to inquiries within a few hours and pre-qualify before scheduling showings.

Examples:

- Pricing example: Your 2BR is listed at $2,200 with minimal inquiries. You pull 10 nearby comps and adjust to $2,095 plus a pet fee. Lead volume increases and you lease faster.

- Lead filtering example: You add three questions to your inquiry form (move-in date, number of occupants, and income minimum). You cut showings by half and still fill the unit.

DIY vs. hire guidance:

- DIY if you can take quality photos, respond quickly, and run showings.

- Hire if you are remote or cannot respond consistently. Vacancy is where "saving a fee" can become expensive.

For the full annual cost stack including placement and renewal fees, see the true cost of hiring a property manager.

3.2 Leasing and Showings (Turning a Prospect into a Signed, Enforceable Lease)

What it involves: Scheduling showings, answering questions consistently, providing applications, collecting holding deposits where legal, drafting lease addenda, and executing signatures.

Typical difficulty and time: Medium; operationally straightforward but detail-heavy.

DifficultyTime per lease cycleLegal sensitivityMedium4-10 hoursMedium-High

Risk if done poorly: Lease mistakes create enforceability problems. Inconsistent statements during showings can also create fair-housing risk.

DIY tools and systems:

- Digital applications and e-signatures

- Template lease package reviewed by a local attorney once, then reused

- Standard house rules addendum covering noise, trash, smoking, and parking

Actionable tip: Write a showing script so every prospect receives the same facts: rent, deposits, screening standards, occupancy limits, and pet policy. Consistency protects you legally and operationally.

Examples:

- Lease execution example: You require renters insurance, list it in the lease and in your move-in checklist, and verify proof before keys are released.

- Showing boundaries example: A prospect asks, "Is this a quiet building?" Rather than making a promise, you explain the building's quiet hours policy and enforcement steps, reducing future disputes.

DIY vs. hire guidance:

- DIY if you can follow a checklist and avoid improvising terms midstream.

- Hire (lease-only) if you dislike showings, travel often, or struggle with documentation.

3.3 Tenant Screening and Selection (Where Most "Bad Tenant" Stories Actually Start)

What it involves: Identity verification, income verification, credit and background checks, rental history review, reference calls, and consistent approval and denial logic.

Typical difficulty and time: Medium; emotionally challenging and administratively repetitive.

DifficultyTime per applicantRisk levelMedium20-60 minutesHigh

Risk if done poorly: The financial downside is significant. Research indicates that stronger screening can reduce eviction rates from 15.8% to 4.1%, with large ROI given that eviction costs typically total $3,500-$10,000. Fair Housing liability can also attach to owners and agents if screening is inconsistent or discriminatory.

DIY tools and systems:

- Written screening criteria covering income multiple, credit thresholds, and conditional approvals

- Integrated credit and background screening through landlord software

- Standardized adverse-action notice workflow

Actionable tip: Decide your criteria before you market. Apply the same criteria every time. That is both smarter and legally safer.

Examples:

- Income verification example: An applicant submits pay stubs. You also request last year's W-2 or an offer letter for new employment and confirm employer contact information before approving based on documented criteria.

- Rental history example: A prior landlord reference is positive, but the phone number traces back to the applicant. You require a property-tax record match or management company verification before counting it.

DIY vs. hire guidance:

- DIY if you can be consistent and comfortable declining applicants with documentation.

- Hire if you are uncertain about Fair Housing requirements, tend to rely on intuition, or feel pressure to bend your own rules.

3.4 Rent Collection and Arrears Management (Systems Beat Awkward Conversations)

What it involves: Payment methods, reminders, late fees where legal, payment plans where appropriate, notices, and delinquency tracking.

Typical difficulty and time: Low to medium with automation; high if you are chasing checks.

DifficultyTime per month per unitBiggest leverLow-Medium10-30 minutesAutopay + clear policy

Risk if done poorly: Cash-flow instability and delayed escalation. Surveys show late or non-payment is common: one landlord survey found 52% of landlords had at least one tenant not pay rent in a given month. Payment automation helps: autopay has been associated with 99% on-time rent versus 87% without it.

DIY tools and systems:

- Online payment portal with autopay

- Automated reminders and receipts

- Ledger that tracks rent, fees, credits, and partial payments

Actionable tip: Make autopay the default expectation. If you allow exceptions, require written requests and set an expiration date on the arrangement.

Examples:

- Autopay example: A tenant enrolls in autopay on move-in day. Late payments decrease and payment uncertainty is eliminated.

- Delinquency workflow example: Day 2 late = friendly reminder; Day 5 late = formal late notice; Day 8 late = legal notice per your state rules. Timelines vary by state.

DIY vs. hire guidance:

- DIY for most small landlords if you use online payments and follow a notice calendar.

- Hire if you dread confrontation or routinely delay sending notices.

3.5 Maintenance and Repairs (The Real Job Is Coordination, Not Fixing Toilets)

What it involves: Intake, triage of emergencies vs. routine issues, vendor dispatch, quotes, approval thresholds, quality control, and preventive maintenance scheduling.

Typical difficulty and time: Medium; spikes with older properties and tenant turnover.

DifficultyTime per month per unitCost variabilityMedium1-3 hoursHigh

Risk if done poorly: Habitability issues, property damage, and tenant dissatisfaction. Maintenance budgets are typically estimated at 1%-4% of property value annually. For a $300,000 property, that is roughly $3,000-$6,000 per year. Under-budgeting leads to deferred repairs and larger failures.

DIY tools and systems:

- Maintenance request portal with photo and video submission

- Vendor list with pricing guidelines and response-time expectations

- Preventive maintenance calendar covering HVAC filters, smoke and CO detectors, and gutter cleaning

Actionable tip: Use an approval threshold: any repair over $300 requires your sign-off; emergency repairs have pre-authorized rules in place.

Examples:

- Triage example: A tenant reports "water under sink." Your system asks for a photo. You identify a loose trap and schedule a handyman, preventing cabinet rot.

- Preventive example: Annual HVAC service reduces peak-season breakdowns and keeps tenants more satisfied.

DIY vs. hire guidance:

- DIY if you have reliable vendors and can respond quickly.

- Hire if you are remote, your building is maintenance-heavy, or you lack vendor relationships.

3.6 Inspections (Move-In, Routine, Move-Out: Documentation Equals Leverage)

What it involves: Condition documentation, safety checks, lease compliance, early detection of leaks and unauthorized occupants or pets, and deposit dispute defense.

Typical difficulty and time: Medium; requires thoroughness more than specialized skill.

Inspection typeTimePayoffMove-in45-90 minSets baseline evidenceRoutine20-45 minCatches issues earlyMove-out45-90 minSupports deposit deductions

Risk if done poorly: Deposit disputes and missed damage. Security deposit rules vary by state, and errors can trigger penalties.

DIY tools and systems:

- Photo checklist by room with cloud storage folder per unit

- Timestamped videos and signed inspection forms

- A repair responsibility chart (tenant vs. landlord) included in your welcome packet

Actionable tip: Conduct a short inspection 60-90 days after move-in. Many chronic issues, such as cleanliness problems or unauthorized pets, appear early.

Examples:

- Move-in baseline example: You photograph every wall, floor, appliance serial plate, and smoke detector. Six months later, any damage claim is clear and unemotional.

- Routine inspection example: You find a slow toilet leak that would have rotted the subfloor. A $25 part prevents a $2,500 repair.

DIY vs. hire guidance:

- DIY if you are local and comfortable being firm but professional.

- Hire if you are remote or conflict-avoidant; inspections require direct conversations.

3.7 Bookkeeping and Owner Reporting (Even If You Are the Owner, You Need "Owner Reports")

What it involves: Income and expense categorization, bank reconciliation, security deposit tracking, monthly statement generation, and tax-ready reporting.

Typical difficulty and time: Low to medium with systems; high if you mix accounts.

DifficultyTime per monthCommon failureLow-Medium1-3 hoursCommingling funds or missing receipts

Risk if done poorly: Tax mistakes, poor decision-making, and difficulty proving deductions. Professional PM operations emphasize standardized financial reporting for exactly this reason.

DIY tools and systems:

- Separate bank account per entity, or at minimum a dedicated rental account

- Receipt capture with expense tagging

- Monthly close checklist: reconcile accounts, review arrears, verify vendor bills

Actionable tip: Run your rentals like a small business. One chart of accounts, one monthly close day, one consistent folder structure.

Examples:

- Monthly close example: On the 3rd of each month you reconcile accounts and export a profit and loss report by property. You spot rising plumbing costs and schedule a proactive inspection.

- Deposit tracking example: You record deposits as liabilities, not income, and track them by tenant to avoid accidental spending.

DIY vs. hire guidance:

- DIY if you are organized and willing to do a monthly close.

- Hire a bookkeeper or CPA if receipts pile up or you dread reconciliation. Outsourcing this function is often high-ROI.

3.8 Legal Compliance (Fair Housing, Disclosures, Habitability: Where "I Didn't Know" Does Not Help)

What it involves: Fair Housing compliance, consistent screening criteria, required disclosures, lease legality, deposit timelines, habitability standards, notice requirements, and record retention.

Typical difficulty and time: Medium; requires ongoing vigilance.

DifficultyTimeStakesMediumOngoingVery high

Risk if done poorly: Fair Housing violations, lawsuits, fines, or forced policy changes. HUD's Fair Housing Act framework prohibits discriminatory practices and extends liability broadly to owners and agents. Property managers emphasize training and standardization because compliance is not optional.

DIY tools and systems:

- Written screening criteria with documented decisions

- A reasonable accommodation and modification request workflow

- A disclosure checklist customized to your state and property type

Actionable tip: Build a compliance binder (digital is fine) that includes your criteria, templates, disclosure receipts, notices, inspection reports, and communication logs in one place.

Examples:

- Consistency example: Two applicants request exceptions to your pet policy. You use the same documented process for each request rather than making a judgment call during a showing.

- Recordkeeping example: You keep every adverse-action notice and screening result for a set retention period. If questioned later, you can demonstrate that non-discriminatory criteria were applied consistently.

DIY vs. hire guidance:

- DIY if you are willing to learn your state rules and maintain strong records.

- Hire for attorney review and occasional consultations if you are uncertain. One consultation can prevent a much more expensive error.

3.9 Evictions and Dispute Escalation (The Point Where DIY Can Get Costly Fast)

What it involves: Serving correct notices, documenting non-payment and lease violations, filing in court, attending hearings, coordinating legal lockout where applicable, and managing post-judgment collections.

Typical difficulty and time: High complexity and high stress.

DifficultyTimeFinancial exposureHigh5-20+ hoursHigh (often $3,500-$10,000)

Risk if done poorly: Procedural mistakes reset the clock, increase lost rent, and can create liability. Strong screening is your first line of defense: research shows that improved screening can dramatically reduce eviction frequency.

DIY tools and systems:

- A delinquency timeline and documentation log

- Notice templates that match your state and city rules

- A relationship with a landlord-tenant attorney established before you need one

Actionable tip: Decide in advance what triggers escalation, such as "file on Day X if unpaid." Wavering prolongs losses.

Examples:

- Non-payment case: A tenant pays partial rent repeatedly. Without a policy, you accept partials and delay action. With a policy, you follow a structured notice-and-file timeline.

- Lease violation case: An unauthorized occupant is documented through inspection and communications. You issue a cure notice and track compliance; if not cured, you escalate.

DIY vs. hire guidance:

- DIY only if you have strong local procedural knowledge, time for court appearances, and a high tolerance for process.

- Hire in most cases. An attorney or experienced eviction service is often cheaper than a failed filing.

If eviction complexity is your main concern, use the when to hire a property manager decision framework.

DIY vs. Hire: Where Most Small Landlords Land

FunctionDIY works best whenHire or outsource whenMarketingYou respond fast and can do showingsYou are remote or slow to respondLeasingYou are checklist-drivenYou dislike showings or paperworkScreeningYou follow written criteriaYou rely on gut feelRent collectionYou use autopayYou delay notices or accept chaosMaintenanceYou have vendors and availabilityYou are remote or maintenance-heavyInspectionsYou are local and firmYou avoid conflict or travel oftenBookkeepingYou do a monthly closeReceipts pile up or commingling is a riskComplianceYou document consistentlyYou are unsure about HUD and Fair HousingEvictionsYou know procedure coldAlmost everyone else

A DIY Property-Management Operating System You Can Copy

Use this checklist to run your rentals with the structure of a professional manager without becoming one.

A. Marketing system

- Listing template covering features, fees, pet policy, and screening criteria

- Photo checklist covering every room and mechanicals

- Lead tracker with date, time, response, and showing scheduled

B. Leasing system

- Showing script with consistent answers

- Digital application and e-signature workflow

- Move-in packet covering utilities, maintenance request process, and house rules

C. Screening system

- Written criteria covering income, credit, and rental history

- Standard verification steps: ID, income, and landlord reference

- Adverse-action notice process, documented

D. Rent collection system

- Online payments with autopay encouraged

- Late notice calendar with dates and templates

- Monthly ledger review

E. Maintenance system

- Request portal requiring photos and video

- Vendor list with pricing guardrails

- Preventive maintenance calendar for quarterly and annual tasks

F. Inspection system

- Move-in photos and video with signed checklist

- 60-90 day check

- Move-out checklist tied to deposit deductions

G. Bookkeeping system

- Separate accounts with receipt capture

- Monthly reconciliation and profit and loss report by property

- Deposit tracking recorded as a liability, not income

H. Compliance system

- Disclosure checklist with signed receipts

- Fair Housing consistent criteria based on HUD guidance

- Communication log covering all key events

I. Dispute and eviction system

- Escalation triggers and timelines documented in advance

- Attorney contact saved before it is needed

- Document folder: notices, ledger, communications, and inspections

Frequently Asked Questions

What does a property manager do that most landlords underestimate?

Property managers provide two underestimated advantages: consistent systems and measurable performance tracking. Most landlords can complete individual tasks but do not always apply them the same way each time. PMs track metrics like days-to-lease and maintenance response time and run repeatable processes rather than one-off decisions. That consistency matters most in tenant screening and legal compliance, where variability introduces the most risk.

Is self-managing worth it financially?

Self-managing can be financially worthwhile if you replace a property manager's structure with your own documented systems. Full-service management typically costs 8-12% of monthly rent plus leasing and renewal fees. However, one avoidable eviction ($3,500-$10,000) or prolonged vacancy (averaging $3,872 in turnover costs) can erase multiple years of saved fees. The financial case for DIY depends entirely on the quality of your systems.

What is the safest hybrid approach to property management?

A practical hybrid approach handles high-frequency, lower-risk tasks yourself while outsourcing high-stakes functions. Self-manage rent collection with autopay and basic maintenance coordination. Outsource tenant placement if showings and screening drain your time. Hire a bookkeeper or CPA for clean financial records. Retain a landlord-tenant attorney for eviction escalations. This structure keeps you in control of cash flow while protecting against the most costly mistakes.

How many units can one person realistically self-manage?

There is no universal unit threshold for self-management capacity. The real constraint is typically maintenance coordination and leasing during turnover, not raw unit count. Capacity depends on property condition, tenant quality, and the strength of your systems. Consistently missing maintenance calls, delaying repairs, or falling behind on bookkeeping are reliable signals to outsource specific functions before problems compound.

Make Your Decision in 30 Minutes

Pick your next step based on your biggest risk:

- If you fear vacancy: build a listing template and lead tracker and commit to same-day responses.

- If you fear non-payment: turn on online payments and push autopay. Data consistently shows much higher on-time payment rates with autopay in place.

- If you fear legal trouble: write your screening criteria and have your lease and disclosures reviewed once by a local attorney, then standardize.

Then decide: DIY, hybrid, or full-service. Not based on anxiety, but based on which systems you are ready to run.

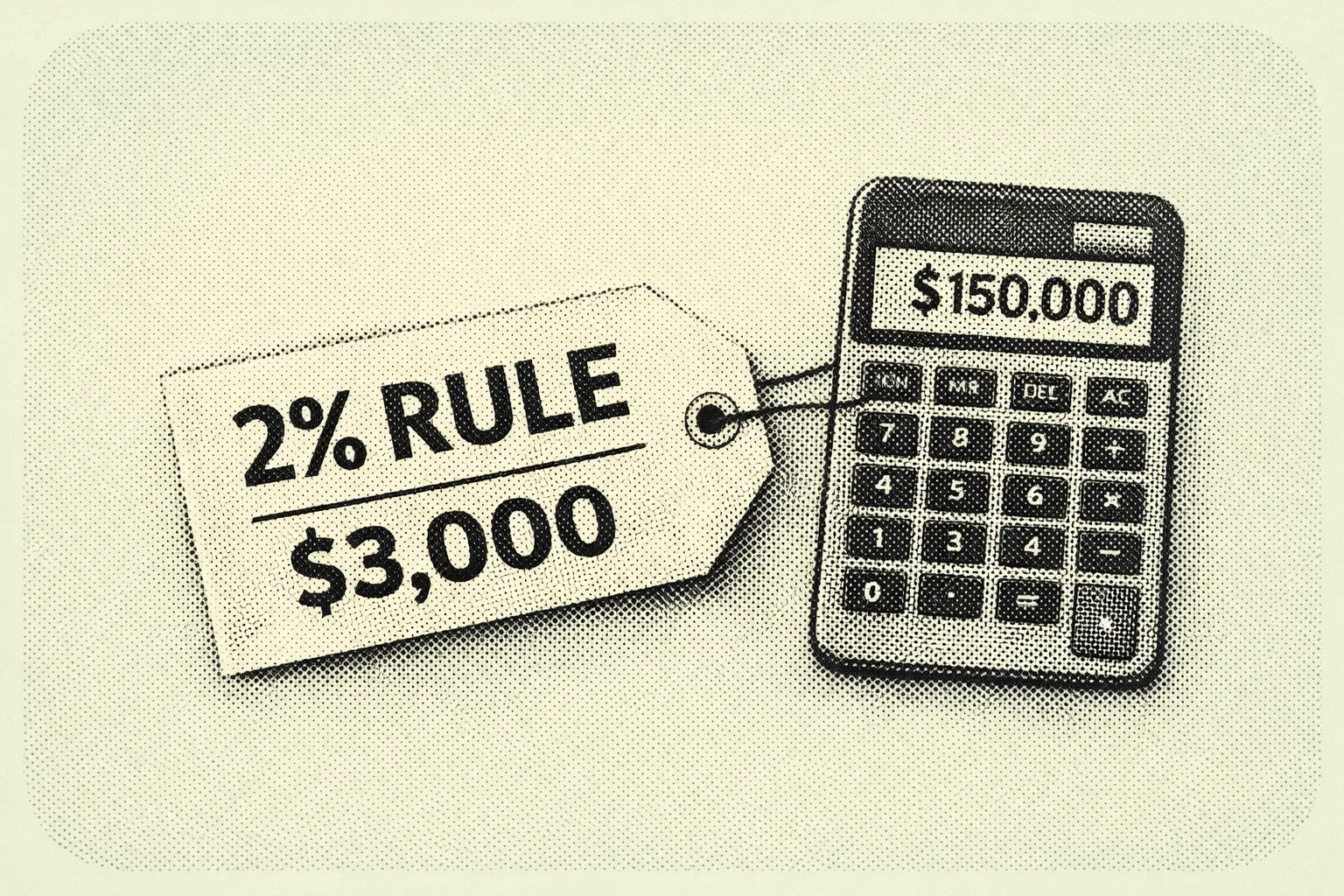

What Is the 2% Rule in Rental Property?

When you self-manage a portfolio, even just a few units, the hardest part of buying a rental property is not finding listings. It is filtering dozens of maybe deals down to the few worth your time. Between listing photos, rough rent estimates, shifting interest rates, and market headlines, you can burn hours underwriting properties that were never going to cash flow.

That is why rent-to-price rules of thumb exist. They are not meant to replace real analysis. They help you triage: move quickly, rule out obvious mismatches, and focus your energy where you will get the best return. Among these quick filters, the 2% rule is the most aggressive.

The formula is simple. A property's monthly gross rent should be at least 2% of your total acquisition cost, meaning purchase price plus rehab. If you buy for $150,000 all-in, you would want $3,000 per month in rent.

The catch is that after post-2020 home price increases, the classic 2% benchmark is now rare in many U.S. metros, especially coastal and high-growth markets. That does not make it useless. It means you need to understand when it works, where it breaks, and what to do next once a property passes or fails the screen.

What the 2% Rule Is and What It Is Not

The 2% rule is a rent-to-cost test: a quick rental income metric that compares gross monthly rent to what you invested to acquire the property. Most definitions specify total acquisition cost as purchase price plus rehab needed to get the unit rent-ready. In real-world underwriting, you will often also want to consider closing costs, initial leasing costs like paint and lock changes, and immediate safety or code items.

The higher the monthly rent is relative to what you paid, the more room you typically have to cover operating expenses including taxes, insurance, repairs, vacancies, and property management, and still produce cash flow. That is why percentage rules became popular among cash-flow investors in lower-cost Midwestern markets and why they have been widely discussed in landlord education communities since the early 2000s.

Here is what the 2% rule does not do. It does not account for local expense structures, which can vary dramatically by county and state. It does not incorporate financing terms including interest rate, down payment, or loan structure. It does not measure profitability directly because it ignores vacancy, maintenance, capital expenditures, and tenant turnover. And it does not capture appreciation expectations, which research has shown can be a major component of long-run returns.

Because of those omissions, the 2% rule is a fast smell test, not a full inspection. Use it as a starting filter, then validate the deal with expense-based metrics like cap rate, cash flow projections, and debt service coverage analysis.

How to Use the 2% Rule Without Fooling Yourself

Step 1. Start With the Exact Formula and Define Your All-In Cost Up Front

The calculation is straightforward.

Rent-to-cost ratio = Monthly gross rent divided by total acquisition cost.

A property meets the 2% rule if monthly gross rent is at least 2% of total acquisition cost.

Run the metric two ways for consistency. The core test uses purchase price plus rehab, which aligns with the most common definition. The conservative test adds estimated closing costs and initial leasing expenses, which is closer to your true cash invested. Rules of thumb are already blunt instruments. If your inputs vary deal to deal, the rule produces noise instead of signal.

Step 2. Use Current Market Anchors to Set Realistic Expectations

The biggest reason landlords get discouraged by the 2% rule is that they apply it in markets where it is structurally unlikely. Recent Zillow data illustrates why this matters.

Los Angeles shows average home values near $941,985 and average rents around $2,658, producing a rent-to-value ratio of roughly 0.28% per month. Seattle shows average home values near $848,869 and average rents around $2,258, producing roughly 0.27% per month. Indianapolis shows average home values near $223,231 and average rents around $1,463, producing roughly 0.66% per month. Cleveland shows average home values near $113,669 and average rents around $1,250, producing roughly 1.10% per month. Tampa shows average home values near $369,079 and average rents around $2,213, producing roughly 0.60% per month.

These are broad metro averages, not deal-specific comps. But they illustrate a critical point: the same 2% threshold implies dramatically different feasibility depending on local prices, rent ceilings, and supply and demand conditions.

Instead of asking whether a market meets 2%, ask what rent-to-cost ratios are typical there, and if 2% is unrealistic, what threshold reliably indicates a workable cash-flow candidate. Many modern investor discussions treat 1% or even 0.8% as more realistic in many areas, while still using 2% as a home-run screen in low-cost or distressed value-add contexts.

Step 3. Run the Calculation Step-by-Step: A Midwest Value-Add Example

A landlord finds an older house in the Cleveland area priced below the broader metro average, needing moderate rehab.

Purchase price: $95,000. Rehab to rent-ready: $15,000. Total acquisition cost: $110,000. Expected monthly gross rent: $1,950.

Dividing $1,950 by $110,000 produces a ratio of 1.77% per month. To meet the strict 2% rule, the property would need $2,200 per month in rent.

This property fails the 2% threshold, but it is close. In many real-world scenarios, a 1.7% to 1.8% ratio may still be worth full underwriting, especially if the rehab estimate is tight, tenant demand is strong, and the neighborhood risk profile fits your management capacity. Cleveland's broader metro average produces about 1.10% rent-to-value. A deal at 1.77% is significantly above that average, suggesting a favorable purchase basis, above-average achievable rent, or both. That is often what a good deal looks like in a low-cost market: you are outperforming the typical rent-to-price relationship, not chasing a mythical 2% in every zip code.

Step 4. Contrast With a High-Cost Coastal Market

A landlord evaluates a small duplex in Los Angeles with strong tenant demand but a high acquisition cost.

Purchase price: $950,000. Rehab and turnover work: $25,000. Total acquisition cost: $975,000. Expected monthly gross rent for both units combined: $5,400.

Dividing $5,400 by $975,000 produces a ratio of 0.55% per month. To meet the 2% rule, the property would need $19,500 per month in gross rent, which is far beyond typical long-term rents for most small multifamily properties in any market.

In coastal markets, investors often justify acquisitions through a different return mix: lower current yield paired with potential long-term appreciation, rent growth, tax advantages, and inflation hedging. Academic work on rent-price dynamics confirms that expected capital gains can heavily influence buying behavior even when rent ratios are low. That is precisely why simplistic ratios can mislead if treated as universal laws rather than market-relative tools.

Step 5. Compare the 2% Rule to the 1% Rule

The 1% rule is the more commonly cited version: monthly gross rent should be at least 1% of total acquisition cost. It became widely popular through mainstream landlord education and investor communities and is generally treated as a first-pass filter before deeper underwriting.

The practical difference comes down to thresholds. The 2% rule is a very high bar, often indicating a low purchase price relative to rent, significant distress or value-add, or a higher-risk area where prices are low for a reason. The 1% rule is still a strong quick screen in many markets but is challenging in most coastal metros given current pricing.

Use both as a funnel. If a deal meets 2%, treat it as a priority but scrutinize neighborhood quality, tenant demand, and deferred maintenance, because too good can mean hidden risk. If it meets 1% but not 2%, underwrite it because it may still cash flow depending on expenses and financing. If it fails 1%, do not automatically discard it in expensive markets, but require a strong alternative thesis: appreciation potential, development optionality, ADU value, or a clear repositioning plan.

Step 6. Cap Rate Versus the 2% Rule: What Each Metric Tells You

Both metrics compress a deal into a single number, but they answer different questions.

The 2% rule uses gross monthly rent and acquisition cost, ignores expenses and financing, and is best as a fast screening tool. Cap rate uses net operating income divided by purchase price, which means it reflects operating reality more accurately because it accounts for taxes, insurance, repairs, management, and other operating costs. Cap rate still ignores financing, but it captures the expense differences that the 2% rule cannot see.

Two properties can have identical gross rent and identical acquisition cost but wildly different cap rates if one sits in a high-tax county, a higher-insurance region, or a property with major capital expenditure coming due. A practical workflow for self-managing landlords: use the 2% or 1% rule to filter, then estimate a quick cap rate to sanity-check the operating story, then run full financing and cash flow projections including cash-on-cash return, debt service coverage, and stress tests.

Step 7. Add Market and Property-Type Nuances

Property taxes and insurance can break a deal that passes the 2% screen. Expense structures vary by location and are not captured in a gross-rent ratio. Never buy the ratio without validating expenses first.

Post-2020 pricing has made 2% rare in many markets. Many landlords now operate with a tiered target: 2.0% as exceptional, typically limited to value-add, distressed, or very low-cost market scenarios; 1.0% to 1.5% as the more common cash-flow hunting range in many non-coastal markets; and 0.5% to 0.9% as common in high-cost metros requiring a different investment thesis.

Property type also matters. A duplex or fourplex may produce more rent per dollar of purchase price than a comparable single-family in the same neighborhood. Some high-demand single-family neighborhoods command a rent premium, but purchase prices often outpace rents, pushing ratios down. Broad Zillow averages in Los Angeles and Seattle confirm this dynamic at the metro level.

2% Rule Quick Screen Template

Use this when scanning listings or reviewing off-market leads. Apply the same inputs and the same math consistently so you do not treat deals differently based on how much you like them.

Inputs: Purchase price. Rehab to rent-ready. Closing and initial leasing costs (optional but recommended). Projected monthly gross rent.

Calculations: Core all-in cost equals purchase price plus rehab. Core rent-to-cost ratio equals monthly rent divided by core all-in cost. Conservative all-in cost adds closing and initial costs. Conservative rent-to-cost ratio equals monthly rent divided by conservative all-in cost.

Decision rules: At 2.0% or above, flag as priority and proceed to full underwriting, but scrutinize neighborhood quality, deferred maintenance, and confirmed rent comps. Between 1.0% and 1.99%, underwrite the deal because it may be viable depending on expenses and financing. Below 1.0%, proceed only with a clear alternative thesis covering appreciation, redevelopment potential, exceptional rent growth, or a positioning plan that supports the acquisition at that price.

Next numbers to pull before making an offer: Rent comps for the same bedroom and bathroom count in similar condition. Taxes and insurance estimates using local sources rather than national averages. A rough annual expense budget covering maintenance, reserves, and vacancy. A quick cap rate calculation to compare against what the rent-to-cost ratio suggests.

Frequently Asked Questions

Is the 2% rule still realistic in 2026?

In many U.S. markets, especially high-cost coastal metros, the traditional 2% rule is rarely achievable for standard long-term rentals because prices have outpaced rent growth. Zillow's broad metro data illustrates the gap clearly: in Los Angeles, average home values near $941,985 paired with average rents around $2,658 produce a rent-to-value ratio far below 1%, let alone 2%. That said, 2% can still appear in specific situations including distressed purchases, heavy value-add rehabs, low-cost neighborhoods, and certain rental operations. Use it as a home-run screen rather than a universal expectation.

Does meeting the 2% rule guarantee positive cash flow?

No. The 2% rule is based on gross rent and acquisition cost and ignores operating expenses and financing entirely. A property can pass the screen and still cash flow poorly if taxes, insurance, maintenance, utilities, or turnover costs are high, or if financing terms are unfavorable. Treat it as the first filter, then validate the deal with expense-based metrics like cap rate and a full financing-based cash flow model.

What is the difference between the 1% rule and the 2% rule?

They are the same concept with different thresholds. The 1% rule says monthly gross rent should be at least 1% of total acquisition cost. The 2% rule uses 2% and is therefore much stricter. In today's pricing environment, many investors view 1% as challenging but sometimes workable in lower-cost markets, while 2% is often limited to unusually strong cash-flow deals or higher-risk areas.

If my market cannot hit 1% or 2%, what should I use instead?