Landlord Challenges

Operational Fixes for the Eight Problems That Cost Landlords the Most

Late rent, vacancy, maintenance, deposit disputes, compliance gaps. The eight problems below repeat at every portfolio size. This hub maps each one to a fix and the system that prevents recurrence.

Landlord Challenges: How One Connected System Solves the Most Common Problems

Landlord challenges are the operational, financial, and legal problems that independent landlords encounter when managing rental properties without staff support or standardized systems. For landlords managing 1 to 20 units, these problems compound quickly: one late payment disrupts your mortgage, one missed maintenance request becomes a habitability issue, and one inconsistent screening decision creates Fair Housing exposure. The most common landlord problems fall into eight categories: tenant screening, rent collection, vacancy, maintenance, security deposits, legal compliance, tenant communication, and financial tracking.

This hub maps each challenge and connects to seven in-depth guides that cover each dimension. Working through these resources gives self-managing landlords the structure to run their rentals with professional-level consistency.

For the broader picture of how professional service standards reduce every one of these challenges, see the standing out as a quality landlord guide.

Three Patterns Behind Most Landlord Problems

Independent landlords rarely fail because they do not care about their properties. They fail because scattered tools create inconsistency, and inconsistency is where risk accumulates.

Fragmented communication means repair requests arrive by text, rent questions come by email, and lease documents live in a folder. When a dispute arises, there is no single record to reference. What was promised, what was completed, and what was documented becomes unclear.

See the tenant communication strategies guide for the centralised communication system that prevents this.

Reactive operations mean marketing starts after a tenant gives notice, renewal conversations happen in the final weeks of a lease, and maintenance gets addressed after a problem escalates. Each of these reactive patterns costs more than the proactive alternative.

See the early lease renewal strategies guide for the proactive renewal workflow that eliminates last-minute vacancy.

Missing documentation is the root cause of most deposit disputes, Fair Housing complaints, and tax problems. Without timestamped photos, written screening decisions, and a complete payment ledger, landlords cannot defend their decisions even when those decisions were correct.

See the landlord documentation best practices guide for the complete file architecture and retention system.

The fix is not working more hours. It is standardizing the workflows that repeat every month so fewer things fall through the cracks.

Eight Landlord Challenge Areas and the Fixes That Stick

1. Tenant Screening and Fraud Prevention

Screening is where most future problems are either prevented or created. Eviction costs commonly range from $3,500 to $10,000 once legal fees, lost rent, and turnover are included. The most controllable lever is upstream: fewer risky placements means fewer downstream conflicts.

Common failure patterns include accepting income documentation without cross-referencing employer details, approving based on intuition rather than written criteria, and applying different standards to different applicants without documentation.

What works:

- Write screening criteria before marketing and apply them the same way every time

- Store screening decisions and denial reasons in one place for Fair Housing auditability

- Verify income documentation against employer contact information, not just pay stub appearance

For the complete breakdown of the 8 most costly screening mistakes and how to fix each one, see the common tenant screening mistakes guide.

2. Rent Collection, Late Payments, and Cash-Flow Stability

Late rent is not just an inconvenience. It is a monthly cash-flow event that, when handled inconsistently, also creates legal risk. Autopay adoption and automated reminders are the single highest-leverage change most small landlords can make to reduce collection friction.

Common failure patterns include collecting by check, accepting partial payments informally without documentation, and sending notices inconsistently based on mood rather than policy.

What works:

- Offer ACH and autopay at lease signing and make it the default expectation

- Send scheduled reminders before the due date, on the due date, and during the grace period

- Keep a payment ledger per tenant that tracks rent, fees, credits, and partial payments in one place

For the step-by-step workflow from first reminder through formal notice and escalation, see the late rent collection strategies guide.

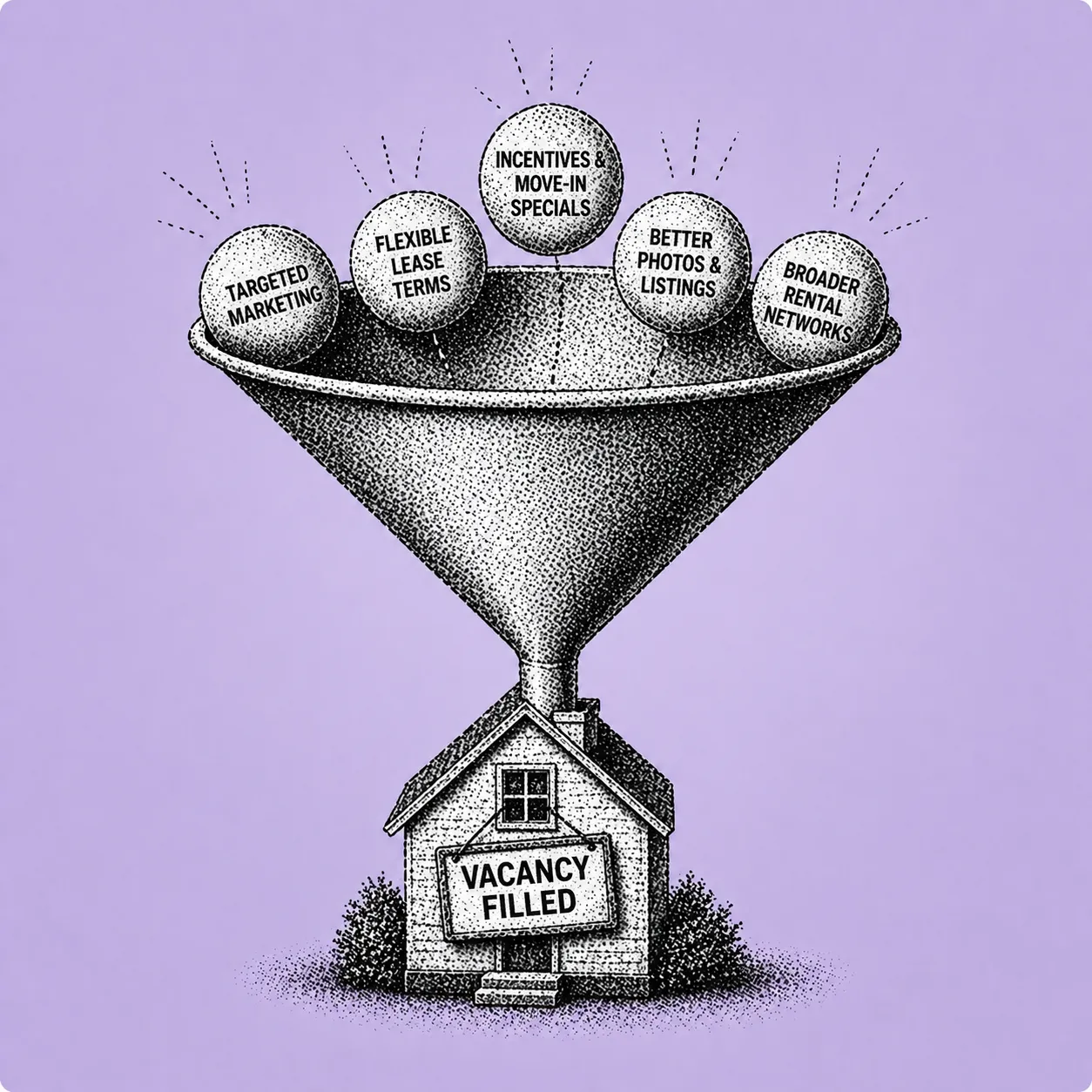

3. Vacancy Risk, Marketing, and Faster Turnovers

Vacancy is both a market condition and an operational problem. National rental vacancy rates have moved upward in recent years, meaning more landlords must market harder while also meeting higher tenant expectations for responsiveness and professionalism. Either way, a repeatable leasing pipeline reduces the time between tenants.

Common failure patterns include starting marketing after a tenant gives notice rather than before, responding slowly to inquiries, and skipping standardized onboarding that sets move-in condition clearly.

What works:

- Use listing templates and prescreen questions to reduce time spent on unqualified inquiries

- Create a turnover checklist with specific dates for cleaning, repairs, photos, listing, and showings

- Track vacancy days per unit as a metric. What you measure improves.

For the complete playbook on reducing vacancy days through faster marketing, better listings, and a continuous tenant pipeline, see the how to reduce vacancy time for rental properties guide.

4. Maintenance Coordination and Cost Control

Maintenance is where landlord time disappears and where small issues become expensive emergencies. Repairs and maintenance commonly represent a significant share of rental income annually, and under-budgeting leads to deferred repairs and larger failures over time.

Common failure patterns include receiving repair requests by text with no photo documentation, using multiple contractors with no shared scope of work, and doing no preventive maintenance scheduling.

What works:

- Route all maintenance requests through one intake channel that captures photos, timestamps, and unit information

- Track time to first response and time to resolution per request

- Schedule seasonal prevention: HVAC servicing, gutter checks, smoke and CO detector testing

For a practical system covering request intake, triage, vendor coordination, and preventive scheduling, see the rental property maintenance guide.

5. Security Deposits, Inspections, and Dispute Prevention

Deposit disputes become expensive when documentation is weak, not necessarily when damage is severe. Move-out conflicts almost always come down to one side saying "it was like that when I moved in" and the other saying "it was not." Dated, labeled photos resolve this before it escalates.

Common failure patterns include skipping a formal move-in checklist, storing inspection photos in a personal phone album with no unit label or date, and providing vague itemization for deductions without invoices.

What works:

- Complete three documented inspections: move-in, optional mid-lease, and move-out

- Store photos with timestamps and a room-by-room checklist tied to the lease record

- Provide tenants with a move-out cleaning checklist 30 to 45 days before lease end

For state-by-state deposit caps, escrow requirements, itemisation deadlines, and move-out documentation workflows, see the security deposit laws by state guide.

6. Legal Compliance and Fair Housing Consistency

Most compliance problems are not intentional. They come from inconsistent processes applied differently over time. Federal and local rules touch advertising language, application decisions, deposit handling, and repair response standards. Details vary by jurisdiction, but the operational fix is the same everywhere: standardize and document.

Common failure patterns include responding to accommodation requests inconsistently, making informal side agreements by text, and deducting from deposits without condition evidence or depreciation rationale.

What works:

- Use templates for notices, lease clauses, and communications, and customize only what is legally appropriate

- Keep a complete paper trail per tenancy: ads, applications, screening outcomes, lease, inspections, repair logs, notices, and payment ledger

- Consult a local attorney for jurisdiction-specific requirements before problems arise

For the complete landlord legal compliance framework covering fair housing, screening, leases, deposits, and documentation, see the compliance and legal hub.

7. Tenant Communication and Conflict De-escalation

Most tenant issues get worse when communication is fragmented or undocumented. When a dispute occurs involving late rent, maintenance delays, or lease violations, the landlord needs a single source of truth: what was reported, what was promised, and what was completed.

Common failure patterns include making verbal commitments during showings, accepting informal texts as official requests, and allowing communication to scatter across multiple channels with no record.

What works:

- Establish a dedicated channel for non-emergency requests and define what constitutes an emergency

- Use message templates for recurring situations: late rent reminders, maintenance scheduling, and lease renewal options

- Summarize phone calls in writing afterward to create a dated record of what was agreed

For the complete framework covering communication channels, response standards, templates, and conflict handling, see the tenant communication strategies guide.

8. Financial Tracking, Taxes, and Profitability Clarity

Many small landlords operate on bank-balance management. If there is money in the account, things feel fine. But profitability depends on vacancy days, turnover costs, maintenance spend, and bad debt. Turnover alone is commonly estimated at $3,000 to $10,000 per unit once make-ready and vacancy loss are included. Without clean records, it is hard to know whether raising rent, deferring upgrades, or changing screening standards is the right move.

For the complete system covering income tracking, expense categorisation, and managing non-paying tenants, see the how to handle delinquent tenants guide.

Common failure patterns include mixing personal and rental expenses, recording maintenance costs annually rather than monthly, and misclassifying capital improvements as operating expenses.

What works:

- Track each property's income and expenses monthly, not annually

- Categorize maintenance versus capital improvements as you go

- Review three metrics quarterly: vacancy days, late-payment rate, and maintenance spend as a percentage of rent

Where the Money Leaks: What the Data Shows

Independent landlords tend to experience challenges as random fires, but the data shows predictable leak points.

Vacancy exposure is both a market and operational problem. Nationally, rental vacancy rates have risen in recent years. Even in tight markets, turnover creates downtime. The operational fix is speed and consistency: faster lead responses, standardized showings, quicker approvals, and e-signed leases.

Late payment friction is reduced materially when you remove friction and timing issues. Online payment adoption has grown significantly over the past decade, and autopay enrollment correlates with higher on-time payment rates. Landlords who default to autopay at lease signing report fewer collection conversations each month.

High-cost outcomes from eviction and turnover are exactly the losses that better screening, earlier intervention, and documented processes aim to prevent. These costs are large enough that preventing even one per year across a small portfolio justifies the time investment in building proper systems.

The practical takeaway is that "better tenants" is not the only lever. Better systems produce measurable improvements in payment reliability, maintenance response time, and dispute outcomes quickly.

{

"@context": "https://schema.org",

"@type": "FAQPage",

"mainEntity": [

{

"@type": "Question",

"name": "What are the most common problems for self-managing landlords?",

"acceptedAnswer": {

"@type": "Answer",

"text": "The most common problems cluster into four areas: cash flow disruption from late rent, vacancy and turnover costs, maintenance coordination breakdowns, and compliance and documentation gaps. These are predictable and recurring. Landlords managing without standardized systems spend more time reacting to each problem than preventing the next one. Prioritizing rent collection automation first addresses the highest-frequency issue."

}

},

{

"@type": "Question",

"name": "How can landlords reduce late rent without damaging tenant relationships?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Use systems that are firm, predictable, and low-friction. Enable online payments and autopay, and send neutral automated reminders before the due date, on the due date, and during the grace period. At lease signing, position autopay as a convenience rather than a requirement. Separate the policy from the tone: consistent enforcement and friendly communication are not mutually exclusive."

}

},

{

"@type": "Question",

"name": "What is the most effective way to prevent security deposit disputes?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Complete a documented move-in inspection with labeled, timestamped photos stored with the lease record and signed by the tenant. At move-out, use an itemized deductions report tied to invoices and dated comparison photos. Provide tenants with a move-out cleaning checklist 30 to 45 days before lease end. Disputes shrink when both sides know what to expect and you can prove condition with evidence rather than memory."

}

},

{

"@type": "Question",

"name": "How much should a landlord budget for maintenance and repairs?",

"acceptedAnswer": {

"@type": "Answer",

"text": "A common starting benchmark is 1% to 4% of property value annually, or roughly $3,000 to $6,000 per year on a $300,000 property. Actual spend depends on property age, tenant wear, and how proactive your maintenance scheduling is. Track maintenance spend as a percentage of rent per property each quarter. A spike in one property is a signal to investigate deferred repairs, vendor pricing, or tenant behavior before the issue compounds."

}

},

{

"@type": "Question",

"name": "Will property management software help if I only have a few units?",

"acceptedAnswer": {

"@type": "Answer",

"text": "Small portfolios often benefit more from software because there is no staff to absorb administrative work. Evaluate software by whether it standardizes your core workflows: screening, lease execution, rent collection, maintenance tracking, and documentation. If automation saves three hours per month, that is 36 hours per year recovered. The value is not in the number of units managed. It is in the consistency delivered across every tenancy."

}

}

]

}

Shuk helps landlords and property managers get ahead of vacancies, improve renewal visibility, and bring more predictability to every lease cycle.

Book a demo to get started with a free trial.

The following guides cover the most common operational, financial, and legal problems independent landlords face. Together they address tenant screening, rent collection, vacancy management, maintenance coordination, deposit disputes, compliance, communication, and financial tracking. Each guide provides practical systems a self-managing landlord can implement without hiring a property manager.

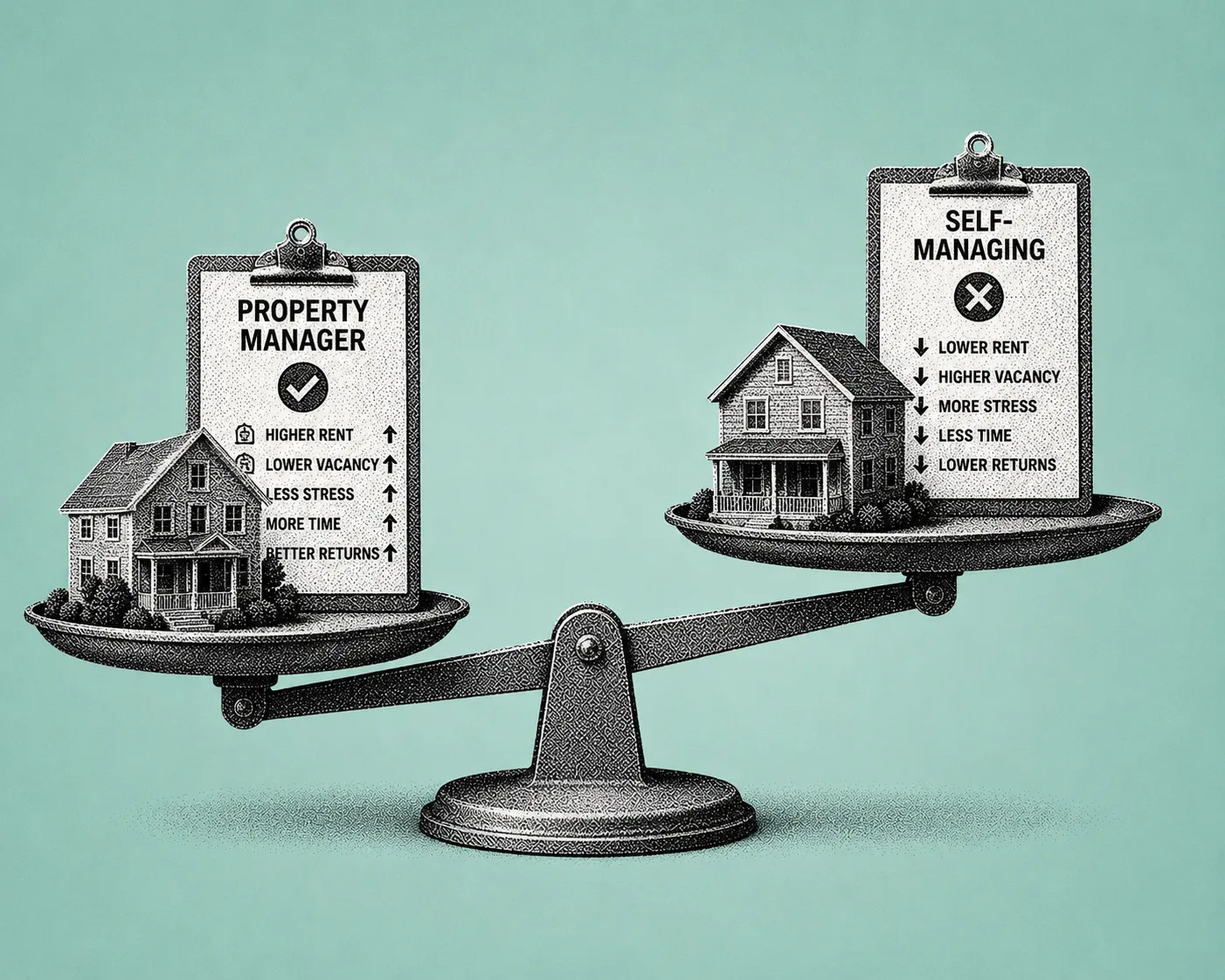

Property Manager vs. Self-Managing: What the Numbers Actually Show

Hiring a property manager looks expensive at first glance. 8% to 12% of gross rent is the typical range, with many contracts landing around 8.5% to 10% nationally. But self-managing is not free either.

The real comparison is total cost. Your time, vacancy days, leasing friction, compliance exposure, maintenance coordination, and the software you need to run rentals predictably.

Most landlords undercount DIY costs because they treat their own labor as "spare time." Yet self-managing commonly takes 8 to 12 hours per property per month. Multiply that by even a modest hourly value and the 8% to 12% fee often is not the problem. Unmeasured operations are.

This guide gives you a numbers-driven framework to compare professional management (fees plus markups plus control tradeoffs) against DIY management (time plus tools plus errors plus opportunity costs), and to calculate break-even unit counts and ROI using a model you can adapt to your portfolio.

What Real Cost Actually Means (and Why Percentages Mislead)

Property management pricing is usually presented as a single number. "10% of rent." In reality, most full-service agreements stack multiple charges.

- Ongoing management: typically 8% to 12% of monthly rent, or sometimes flat $199 to $300 per month.

- Tenant placement or lease-up: commonly 50% to 100% of one month's rent.

- Renewal fees: often around 20% to 25% of one month's rent.

- Setup fees: typically $200 to $500.

- Maintenance markups: commonly around 10%, sometimes more.

- Inspections and eviction admin: inspections around $110 per visit, eviction admin fees sometimes around $500 plus legal costs.

DIY landlords pay differently. They pay in hours and attention. When you self-manage, you still need leasing workflows, tracking, documentation, communication, and compliance. The question is whether you buy those capabilities via a manager, or build them via your time plus software plus processes.

Three things to do before you run the math:

- Stop benchmarking with a single percentage. Build a full-year cost model with turnover and repair assumptions.

- Treat your time as an expense. Even if you enjoy it, it has opportunity cost.

- Compare outcomes, not tasks. The right comparison is net rent collected (after vacancy, fees, repairs) and risk-adjusted headaches.

Step-by-Step: A Numbers-Driven Comparison

Step 1: Calculate the True Cost of Self-Management

Start with the most ignored line item. Your hours. Self-managing landlords commonly spend 8 to 12 hours per property per month on tenant messages, repairs, late rent, bookkeeping, and showings. That is the baseline. Turnovers and emergencies spike it.

DIY cost formula (annual)

- Time cost = hours per unit per month x units x 12 x your $/hour

- Software and tools = subscriptions plus screening plus e-sign plus accounting support

- Vacancy friction = extra vacancy days due to slower leasing or weaker marketing

- Mistake and compliance buffer = late fees not charged, incorrect notices, deposit errors, or preventable disputes. Model as a conservative annual reserve.

For time value, many landlords use what they earn in their job, what it would cost to hire an assistant, or a blended "skilled self-employed" rate. This guide uses $35 per hour as a planning assumption. Swap it for your reality.

Example baseline (per unit)

- Hours: 4 per unit per month (efficient DIY with systems) vs. 10 per unit per month (typical DIY range midpoint).

- Time cost at $35 per hour:

- Efficient: 4 x 12 x $35 = $1,680 per unit per year

- Typical: 10 x 12 x $35 = $4,200 per unit per year

That alone can exceed a manager's fee on many rent levels.

What to do next

- Track your true hours for 30 days. Use a note app and tag tasks (leasing, maintenance, accounting). Your future decision gets easy.

- Separate batch work from interrupt work. Interruptions (calls and texts) are what crush DIY scalability.

- Assign a "stress premium." If you dread tenant messages, your real cost per hour is higher than your spreadsheet says.

Step 2: Model the Full Cost of Professional Management

Professional management usually includes rent collection, maintenance coordination, vendor scheduling, notices, and reporting. But fee structures matter.

Typical annual manager cost components

- Base management fee: 8% to 12% of collected rent.

- Lease-up or placement: 50% to 100% of one month's rent per turnover.

- Renewal fee: around 20% to 25% of one month's rent when renewing.

- Maintenance markup: often around 10% of project cost.

- Other pass-throughs: setup ($200 to $500), inspections (around $110 per visit), eviction admin ($500 plus legal).

Hidden but real costs of hiring a manager

Markup stacking. A 10% maintenance markup can be fine, unless the vendor price is already inflated or repairs are over-scoped.

Less control means slower optimization. You may be slower to upgrade processes, test rent pricing, or implement resident experience improvements.

Incentive mismatches. A percentage fee can align incentives with rent maximization, but also can reduce urgency around cost control. Flat fees create predictability but may reduce upside motivation.

What to do

- Negotiate placement fees. Ask for a flat lease-up fee or a reduced fee on renewals. Placement is where many owners overpay.

- Cap maintenance markup. Put a markup cap in writing and require approval above a dollar threshold.

- Demand a scope plus 3-bid rule above a set amount (for example, $1,000) so convenience does not become silent overspending.

Step 3: Vacancy and Turnover. The Make-or-Break Variable Most Landlords Ignore

Even a strong DIY operator can lose to a good manager if leasing speed and screening quality differ. One extra week vacant is often more expensive than a month of management fees.

Turnover-driven costs to model

- Lost rent during vacancy

- Leasing labor and time (showings, screening, lease prep)

- Placement fees (if managed)

- Make-ready costs (repairs, paint, cleaning)

- Risk of a bad placement (late pays, damage, eviction)

Many managers include marketing in the base fee, but some charge separately. Your model should use your actual contract terms, not averages.

What to do

- Track your days to lease and compare to market norms in your zip code. If you are consistently slower, DIY is costing you.

- Quantify screening misses. One preventable eviction can wipe out years of fee savings. Include a conservative annual error reserve.

- Standardize turnovers. Checklists and templated messages routinely reduce vacancy days, whether you DIY or outsource.

Step 4: Break-Even Analysis: When Does Hiring a Manager Beat DIY?

Below is a practical break-even table using consistent assumptions. You can replace any variable.

Assumptions (editable)

- Average rent: $1,800 per unit per month

- Manager base fee: 10% of rent (midpoint)

- Placement: 75% of one month's rent per turnover (mid-range)

- Turnover rate: 30% per year

- Maintenance spend: $1,200 per unit per year with 10% markup if managed

- DIY time typical: 10 hours per unit per month

- Efficient DIY with software and process: 4 hours per unit per month

- Time value: $35 per hour

- DIY software: $25 per unit per month

Break-even (annual cost per unit)

ModelWhat's includedApprox. annual cost per unitDIY (typical)10 hrs/mo x $35 + software$4,200 + $300 = $4,500DIY (efficient with software)4 hrs/mo x $35 + software$1,680 + $300 = $1,980Professional manager10% mgmt + placement (0.3 x 0.75 mo) + 10% maintenance markup$2,160 + $405 + $120 = $2,685

What this means

- If your DIY workload is near 10 hours per unit per month, a manager can be cheaper per unit even before you price in compliance mistakes or vacancy drag.

- If you can operate at around 4 hours per unit per month with solid systems, DIY is often cheaper, until your unit count grows enough that interruptions break your schedule.

Unit-count break-even (portfolio perspective)

Because both time and most fees scale per unit, the break-even is less about unit count and more about hours per unit and rent level. But unit count matters because DIY hours per unit often rise when you are stretched.

Portfolio sizeDIY typical (10 hrs/unit/mo)DIY efficient (4 hrs/unit/mo)Professional manager4 units$18,000$7,920$10,74020 units$90,000$39,600$53,70060 units$270,000$118,800$161,100

Key takeaway. "Hire a manager at X units" is the wrong rule. The better rule is: if your effective DIY hours per unit per month stay low, DIY wins longer. If you are closer to 8 to 12 hours per unit per month, management often wins early.

What to do

- Calculate hours per unit, not hours total. That ratio is the scalability signal.

- Watch your turnover season. If you self-manage and your leasing months spike your hours, you are underestimating DIY cost.

- Use approval thresholds with managers so the convenience does not inflate maintenance.

Step 5: The ROI Calculator Framework (Plug and Play)

Use this to compare annual net income under both models.

Variables

- U = number of units

- R = monthly rent per unit

- F = manager fee rate (for example, 0.10)

- P = placement fee in months of rent (for example, 0.75)

- T = annual turnover rate (for example, 0.30)

- M = annual maintenance spend per unit

- k = maintenance markup rate (for example, 0.10)

- H = DIY hours per unit per month

- W = your hourly value

- S = DIY software cost per unit per month

- Vd = incremental vacancy days difference (DIY minus manager)

Formulas (annual)

Manager cost (annual) = U x (12 x R x F) + U x (R x P x T) + U x (M x k)

DIY cost (annual) = U x (12 x H x W) + U x (12 x S) + Vacancy impact

Where Vacancy impact = U x (R / 30 x Vd)

Decision metric

- If Manager cost < DIY cost: manager is cheaper, before qualitative factors.

- If Manager cost > DIY cost: DIY is cheaper. Then ask if the extra profit is worth your time and risk.

Worked examples (same assumptions as above, Vd = 0)

4-unit (R = $1,800, F = 10%, P = 0.75, T = 0.30, M = $1,200, k = 10%, W = $35, S = $25)

- Manager: 4 x (12 x 1800 x 0.10) + 4 x (1800 x 0.75 x 0.30) + 4 x (1200 x 0.10) = 4 x 2160 + 4 x 405 + 4 x 120 = $10,740

- DIY typical (H = 10): 4 x (12 x 10 x 35) + 4 x (12 x 25) = $18,000

- DIY efficient (H = 4): 4 x (12 x 4 x 35) + 4 x (12 x 25) = $7,920

20-unit

- Manager: $53,700

- DIY typical: $90,000

- DIY efficient: $39,600

60-unit

- Manager: $161,100

- DIY typical: $270,000

- DIY efficient: $118,800

Now add vacancy differences if you have them. Just 3 extra DIY vacancy days per year (Vd = 3) at $1,800 rent costs about $180 per unit per year (1,800 / 30 x 3), which can quickly erase small DIY savings.

What to do

- Run two DIY scenarios: best month and worst quarter. Most owners decide based on the best month, and regret it during the worst quarter.

- Model placement fee frequency correctly. A placement fee is not monthly. It is turnover-driven.

- Do not ignore renewal fees. If your manager charges renewals (around 20% to 25% of a month), add it.

Step 6: Three Landlords, Three Different Answers

These are realistic, simplified examples using the framework above (numbers are modeled from the fee ranges cited, rents and hours are scenario assumptions).

Case A: 4-unit owner in Dallas (busy W-2 job, high interruption cost)

- Rent: $1,700 per unit, U = 4

- DIY hours: 11 hours per unit per month (newer landlord)

- Time value: $40 per hour

- Manager offer: 10% + 75% placement + 10% maintenance markup

Result. DIY labor alone is approximately 4 x 12 x 11 x 40 = $21,120 per year (before software). Manager base fee is approximately 4 x 12 x 1700 x 0.10 = $8,160 per year. Even after placement and markup, the manager is financially rational because the owner's time is expensive and interruptions are constant.

Case B: 12-unit investor in Phoenix (systems-first DIY, low hours per unit)

- Rent: $1,450, U = 12

- DIY hours: 4 per unit per month (strong templates, batching, reliable vendors)

- DIY software: $30 per unit per month

Result. DIY cost is approximately 12 x (12 x 4 x 35) + 12 x (12 x 30) = $25,920 per year. Manager cost at 10% plus turnover placement can land closer to $30,000 or more depending on turnover. This owner likely stays DIY unless vacancy days creep up or compliance complexity increases.

Case C: 50-unit holder in Indianapolis (portfolio scale, turnover pressure)

- Rent: $1,250, U = 50

- DIY hours: 6 per unit per month baseline, but spikes during summer turnovers

- Turnover: 40%

Result. At this size, the operational bottleneck is not accounting. It is leasing coordination and maintenance triage. A manager's placement fees (50% to 100% of a month) can sting, but if professional operations reduce vacancy by even a few days per turn, the savings can outweigh fees. Many owners here choose a hybrid: outsource leasing and maintenance coordination, keep strategic control.

Your Practical Cost Input Sheet and ROI Box

Use this as a copy-paste template for a spreadsheet.

DIY annual cost inputs

- Units (U): ___

- Average monthly rent per unit (R): ___

- Hours per unit per month (H): ___ (track for 30 days)

- Hourly value (W): ___

- DIY software cost per unit per month (S): ___

- Incremental DIY vacancy days per year (Vd): ___

- Annual mistake or compliance reserve per unit (optional): ___

DIY annual cost = U x (12 x H x W) + U x (12 x S) + U x (R / 30 x Vd) + U x Reserve

Manager annual cost inputs

- Management fee rate (F): ___ (8% to 12% typical)

- Placement fee (P in months): ___ (0.5 to 1.0 typical)

- Turnover rate (T): ___

- Renewal fee (optional): ___ (often 20% to 25% of a month)

- Setup fees (one-time): ___ ($200 to $500 typical)

- Maintenance spend per unit per year (M): ___

- Maintenance markup (k): ___ (often around 10%)

- Inspection fees: ___ (around $110 per visit if applicable)

Manager annual cost = U x (12 x R x F) + U x (R x P x T) + U x (M x k) + other fees

Decision rule (simple)

- If Manager annual cost < DIY annual cost: outsourcing is financially justified.

- If DIY is cheaper, ask: "Is the difference worth the time, risk, and interruption load?"

FAQ

What is a reasonable property management fee in the U.S.?

For full-service residential property management, ongoing fees commonly fall in the 8% to 12% of monthly rent range. Many managers also charge turnover-driven fees like 50% to 100% of one month's rent for placement. Renewal fees often run around 20% to 25% of a month, and maintenance markups around 10% are common. The right comparison is the full annual stack, not the headline percentage.

How long does self-management usually take per unit?

Estimates commonly cited for self-managing landlords are around 8 to 12 hours per month per property. If you have strong systems, batched workflows, and low turnover, you may beat that. If you manage reactively, with no templates and scattered tools, you may exceed it. The single biggest scalability signal is hours per unit, not hours total. Track your real hours for 30 days before you decide.

Are maintenance markups normal with property managers?

Yes. Industry guides frequently note maintenance markups, often around 10% of project cost, as a common practice. The key is transparency, approval thresholds, and limiting markups on large projects. Ask for vendor invoices to be shared, require explicit markup line items, and set an owner-approval threshold above a fixed dollar amount so a 10% markup on a $10,000 project does not happen quietly.

Can management fees and software be deducted?

Many ordinary and necessary rental operating expenses are generally deductible. Property management fees are typically treated as operating expenses in rental accounting practice and reported on Schedule E. For specifics on your situation, consult IRS guidance or a tax professional. Always coordinate with your CPA on fee categorization and any limitations specific to your filing.

What to Do Next

If the math says professional management wins for your situation, hire deliberately. Negotiate placement fees down to a flat amount or a reduced renewal rate. Cap maintenance markups in writing. Set approval thresholds. Require scope and three bids above a fixed dollar amount. Convenience without controls is how the headline 10% becomes the all-in 20%.

If the math says DIY should win, the next step is making DIY reliably efficient, so your hours per unit do not drift upward as your portfolio grows. The break-even tables above show that the difference between 10 hours per unit per month and 4 hours per unit per month is the difference between a manager being cheaper and DIY being dramatically cheaper. That gap is operational discipline. Templates, batched workflows, reliable vendors, and a single connected system instead of scattered tools.

This is exactly what Shuk is built for. Shuk gives systems-first DIY landlords the operational backbone of a property manager without the fees. Online rent collection with zero ACH transaction fees and automatic reminders. Configurable late fees that apply automatically. Tenant screening through our partner. E-signature for leases through our Adobe-powered integration. Maintenance request tracking with photos, documents, and a complete history per property. Centralized in-app messaging with email and push notifications. Schedule E-aligned expense organization. Payment and income reports filtered by property or date range. The Lease Indication Tool polls tenants monthly starting six months before lease end so you get predictive lease renewal insights and reduce the turnover-driven costs this article warns about. Year-Round Marketing keeps your listing current and ready to go live the moment you need it, so vacancy days do not stretch.

At $5 per unit per month with no setup fees, and with White Glove Onboarding included at no additional cost (where the Shuk team handles property setup, account preparation, and renter onboarding for you), Shuk is the systems layer that keeps the hours-per-unit ratio low as your portfolio grows.

Book a demo at shukrentals.com/book-a-demo to see how Shuk's online rent collection with zero ACH fees, automatic reminders, automated late fees, maintenance request tracking, centralized in-app messaging, Schedule E-aligned expense organization, the Lease Indication Tool, and Year-Round Marketing work together so you can self-manage with manager-level process discipline without manager-level fees.

How to Serve Notices to Uncooperative Tenants: A Step-by-Step Playbook

Serving a notice should be simple. Then the tenant stops answering the door, disputes the address, claims they never got it, or runs out the clock with every delay tactic available. For landlords managing 1 to 100 units, this is the moment a predictable operational task can quietly become a high-stakes compliance problem.

In many jurisdictions, a defective notice or improper service can derail an otherwise valid case, even when the tenant clearly violated the lease. The bigger risk is not confrontation. It is procedural failure. Wrong notice type, wrong timeline, wrong amount, or a service method that does not meet statutory requirements.

Courts often treat notice service as a gateway issue. If you cannot prove proper notice and service, you may be sent back to start over and lose weeks of rent and cash flow along the way.

This is not a rare edge case. Eviction Lab reported approximately 3.6 million eviction filings in the U.S. in 2018. With that volume, housing courts see the same avoidable mistakes repeatedly: missed deadlines, incomplete details, improper service, and weak documentation. These are exactly the errors that experienced housing-court practitioners warn lead to dismissals.

This guide gives you a practical, legally grounded workflow to serve notices to uncooperative or evasive tenants in a way that holds up when challenged. Throughout, we will note where centralized communication, maintenance histories, and document storage reduce ambiguity and help you prove what happened, when, and how.

Disclaimer: This article is not legal advice. Notice rules vary by state and city, and they change. When in doubt, especially with rent-controlled units, subsidized tenancies, or "just cause" requirements, consult a qualified local attorney.

What "Proper Service" Really Means

A notice is more than a piece of paper. It is a legal trigger that starts a timeline. If you serve it incorrectly, your next step (often an eviction filing) can be delayed or dismissed even if the tenant clearly violated the lease. Housing-court best-practice resources emphasize precision, clarity, and documentation, especially around service and recordkeeping.

Two frameworks shape the rules you must follow.

Federal overlays (when applicable)

For certain federally backed properties, Section 4024 of the CARES Act created a requirement to provide at least 30 days' notice to vacate after the moratorium period and restricted certain nonpayment evictions during the covered timeframe. Separately, federally assisted programs like Housing Choice Vouchers have their own termination and notice requirements under 24 CFR § 982.310. Even small operators can be subject to these rules depending on financing or subsidy involvement.

State and local service rules

Most day-to-day notice service requirements come from state statutes and court procedures. California is a clear example. California Code of Civil Procedure § 1162 lays out methods including personal service, substituted service, and "post and mail" (posting plus mailing). California also has separate termination notice timelines, often 30 or 60 days depending on tenancy length, under Civil Code § 1946.1.

The rest of this guide walks the workflow: choose the correct notice and service method, draft and deliver notices with court-ready proof, handle evasive tenants, and know when to escalate to a process server or attorney.

Step 1: Verify Your Legal Grounds and Pick the Correct Notice Type Before Drafting Anything

The fastest way to lose time is to serve a beautifully formatted notice for the wrong legal reason. Start by confirming what you are noticing and what outcome you are requesting.

Common grounds (varies by state and local law):

- Nonpayment of rent (pay-or-quit)

- Curable lease violation (cure-or-quit)

- Non-curable breach (quit)

- Termination or non-renewal, often 30 or 60-day notices depending on facts

- Program-specific termination, like voucher-related rules under federal regulations

Federal check (do not skip this)

If your property is covered by CARES Act protections, like certain federally backed mortgages during the relevant period, the CARES Act required at least a 30-day notice to vacate in covered scenarios.

If your tenant is in a Housing Choice Voucher arrangement, review 24 CFR § 982.310 on owner termination requirements. A standard notice you used for market-rate tenants may be insufficient.

State example: California timeline

California generally requires 30-day or 60-day termination notices depending on how long the tenant has resided in the unit, under Civil Code § 1946.1. Serving the wrong length can undermine the next step.

Practical tip: treat this like a mini-audit

- Pull the signed lease and ledger

- Confirm tenant names and unit address exactly as in the lease

- Confirm the violation date or dates and whether the issue is curable

- Confirm any federal program or financing overlays

Example scenario

A tenant stops paying rent and emails that they are withholding due to a leaking ceiling. The landlord is ready to serve a nonpayment notice immediately. But the maintenance history shows the tenant first reported the leak two weeks ago and no vendor was dispatched. The landlord pauses to triage repairs, documents the work order, and then serves the correct notice with clean records. The maintenance workflow prevents an avoidable retaliation or habitability narrative.

Step 2: Draft a Notice That Is Accurate, Specific, and Updated to Current Rules

Courts expect notices to be precise. "Close enough" is where dismissals happen.

Drafting essentials

- Correct legal names of tenants matching the lease

- Full property address and unit number

- Clear reason for the notice including what happened and when

- Exact deadline to comply or vacate, calculated carefully

- Exact amount demanded for nonpayment notices, plus how and where to pay

- Signature, date, and landlord or agent contact info

- Required statutory language, which varies by state and local rules

California cautionary tale on precision

California courts have demonstrated strict standards on three-day notices. Reported cases include dismissal risk over small discrepancies in rent demands, including one example involving a $4.44 mismatch. Other California decisions have emphasized that three-day notices must be clear and include proper dates and unambiguous terms or they may be challenged as defective. The lesson: a small calculation error can cost weeks.

Actionable drafting tips

- Pull amounts from your ledger, not memory

- Separate base rent from fees if your jurisdiction limits what can be demanded in a pay-or-quit (legal specifics vary)

- Use a current template that matches current statutes and case law. Do not reuse a 2019 form blindly.

Example scenario

A landlord prepares a three-day notice using an old spreadsheet and accidentally includes a small late fee that was not authorized under the lease. The tenant's attorney challenges the notice as defective. The landlord must re-serve and restart the clock. Pulling rent figures from a clean centralized ledger and stored lease addenda would have reduced the risk of a mismatch between the notice amount and the contract terms.

Step 3: Choose a Legally Valid Service Method and Do It Exactly as Required

Many landlords focus on the content of the notice and underestimate service rules. But service is often where evasive tenants create the most friction and where courts look for strict compliance.

California example: CCP § 1162 service methods

California law provides specific ways to serve a notice:

- Personal service (deliver to tenant directly)

- Substituted service (deliver to a person of suitable age and discretion at residence or business, plus mailing)

- Posting and mailing ("nail and mail," meaning post conspicuously and mail a copy)

These are laid out in California Code of Civil Procedure § 1162, and California courts provide public self-help guidance on how to deliver notices.

Practical selection guidance (generally applicable)

Try personal service first when safe and feasible. It is the cleanest proof.

If the tenant dodges the door, substituted service may be available depending on your jurisdiction, but follow every step including the required mailing.

Posting plus mailing is often allowed only after due diligence attempts at personal or substitute service (jurisdiction-specific). Do not jump to posting just because it is convenient.

Electronic notice

Electronic delivery is evolving and varies widely. Some jurisdictions have begun authorizing opt-in electronic delivery in certain contexts. Florida, for example, created an opt-in electronic notice statute. But many areas still require traditional methods unless the statute or lease allows otherwise. Treat e-delivery as a supplement unless your local rules clearly authorize it for the specific notice type.

Example scenario: the evasive-tenant pattern

A tenant never answers the door, ignores calls, and removes posted papers. The landlord makes three documented personal-service attempts at different times, then uses the legally permitted posting-and-mailing method. Because every attempt is logged and backed by photos and mailing proof, the tenant's "I never received it" claim has less traction. A unified timeline of communication, photos, and documents makes the story easy to present consistently in court.

Step 4: Document Delivery Like You Expect to Be Challenged

If a tenant is uncooperative now, they may later claim the notice was never served or served improperly. Your goal is to make your service provable, repeatable, and credible.

Documentation you should capture

- A copy of the exact notice served (final version)

- Date and time of each service attempt and method used

- Who served it (name and relationship: owner, agent, process server)

- Where it was served (address, unit door, mailbox, etc.)

- For posting: clear photos showing placement in a "conspicuous place"

- For mailing: certificate of mailing or postal receipt, depending on your method

- Any proof-of-service declaration required or recommended

California landlords often use a Proof of Service or Declaration of Service to memorialize how notices were delivered. Courts and practitioner materials repeatedly stress that procedural errors, especially around notice and service, are a major reason landlords lose time in housing court.

Two data points to keep your team focused. Eviction Lab's research indicates eviction filings remain a high-volume feature of U.S. housing, with about 3.6 million filings in 2018. High volume often means high scrutiny of "routine" procedural steps. Housing-court analyses aimed at landlords emphasize that landlords frequently lose on technicalities like defective predicate notices and service problems. Treat "service failures are common" as the operating assumption.

Pro tip

If you ever end up in court, you want to avoid "I think it was on Tuesday." You should be able to say: "It was served Tuesday at 6:42 p.m. by substituted service to [name], and a copy was mailed the same day," with attachments ready.

Step 5: Handle Evasive Tenants With Lawful Tactics That Reduce Drama

Evasive tenants typically rely on two things: your impatience and your lack of documentation. The fix is a calm, repeatable playbook.

Lawful tactics (general best practices, verify locally)

- Vary the time of attempts. Try morning, early evening, and weekend. Courts like to see reasonable diligence.

- Bring a neutral witness, not a co-tenant. Your witness can later sign a statement.

- Use substituted service correctly if your state permits it. Serve a responsible adult at residence or business and complete any required mailing steps. California's CCP § 1162 contemplates substituted service plus mailing.

- Use posting plus mailing only when allowed. Posting alone is rarely sufficient. California's statute requires posting and mailing for that method.

- Do not self-escalate into harassment. Repeated knocking for hours, threats, or improper entry can create counterclaims. Keep communications professional and documented.

California case pattern: notice challenged due to defective service

California cases and practice materials show that tenants can challenge defective service through motions that attack how the notice was delivered, including motions to quash based on improper notice service. The practical lesson: even if the tenant "obviously knew," the court may still require strict compliance with statutory service steps. If your tenant is already evasive, assume they will use every procedural defense available.

Success story: process server plus post-and-mail done right

A property manager faces a tenant who never answers and has a ring camera but will not engage. After two documented attempts, the manager hires a process server experienced in the jurisdiction's posting-and-mailing rules. The server completes the posting with photos, completes the mailing with documented proof, and signs a detailed declaration. The tenant still claims non-receipt, but the court accepts the service proof and the case proceeds without restarting the notice clock. Strong, credible proof of service defeats "never received" narratives.

Step 6: Know When to Escalate to a Process Server or Attorney

Independent landlords often try to do everything themselves. That can work until the tenant is sophisticated, represented, or simply committed to delay. The cost of starting over can exceed the cost of hiring help early.

Escalate to a process server when

- The tenant is evasive, will not answer, will not accept, or removes postings

- You need third-party credibility for proof of service

- You have safety concerns about face-to-face service

- Your local rules require a non-party to serve certain documents (common in some stages, verify locally)

Escalate to an attorney when

- The tenant is subsidized and voucher rules may apply under 24 CFR § 982.310

- You suspect CARES Act coverage or other federal overlays apply

- You are in a highly regulated area like rent control, just-cause, or relocation assistance, which is often local

- The tenant has raised habitability, discrimination, or retaliation allegations

- You have already had one notice rejected or challenged. Do not repeat the mistake.

Practitioner resources repeatedly emphasize that landlords lose housing court cases on avoidable technicalities including defective predicate notices, improper service, missing documentation, or inconsistent records. If you are operating 1 to 100 units, a single dismissed case can erase months of cash flow.

The strategic goal is not "be tougher." It is "be cleaner" legally and procedurally so the tenant has fewer opportunities to stall.

Notice Service Checklist (Use This Every Time)

Use this checklist every time you serve a notice, especially with difficult tenants. Turn it into a saved workflow and attach evidence as you go.

A. Pre-notice verification

- Confirm tenant legal names and unit address match lease

- Confirm grounds (nonpayment, breach, termination) and dates

- Confirm amount due from ledger, no guesses

- Check federal overlays: CARES Act coverage if applicable, voucher termination rules if applicable

- Check state timeline requirements, like California's 30 or 60-day termination under Civil Code § 1946.1

B. Draft the notice

- Use a current template, avoid outdated forms

- State reason clearly and specifically

- Include correct deadline and compliance instructions

- Save the exact final version served as a PDF

C. Choose service method

- Confirm allowed service methods in your state (CCP § 1162 in California)

- Attempt personal service first if safe

- If using substituted service, complete the required mailing step

- If using posting, also mail where required (California requires posting plus mailing for that method)

D. Document everything

- Log each attempt: date, time, location, method

- Take photos, especially for posting

- Keep mailing receipts

- Complete proof or declaration of service (recommended, common in California practice)

- Store all evidence in one organized place

E. Post-service

- Send a professional in-app message confirming service attempt details as a supplemental record

- Calendar the deadline and the next decision point

- If the tenant disputes service, prepare your service packet for counsel

FAQ

Can I serve notices by email or through an app instead of delivering paper?

Sometimes, but only when your jurisdiction allows it for that notice type or when the tenant has validly opted in under applicable law. Florida has created an opt-in pathway for electronic delivery of certain landlord-tenant notices, but many jurisdictions still require personal, substitute, or post-and-mail service for core eviction notices. Treat electronic delivery as a supplement, not a replacement, unless you have verified the local rule.

What if the tenant claims they never received the notice?

This is exactly why proof matters. Courts typically focus on whether you complied with the authorized service method and can prove it, not on whether the tenant admits receipt. Use photos for posting, mailing receipts, and a detailed proof or declaration of service. Preserve your time-stamped in-app messages as supporting evidence of your efforts and professionalism.

How soon can I file after serving the notice?

It depends on the notice type and jurisdiction. Some notices create short cure periods. Termination notices can run 30 or 60 days, as in California under Civil Code § 1946.1. Federal overlays can also affect timing, like the CARES Act 30-day notice requirement for covered properties. The practical rule is do not file until the statutory period fully expires, and calendar the deadline carefully.

When is it worth paying for a process server?

If the tenant is evasive, if you anticipate a contested case, or if your prior attempts are already messy, a process server can pay for itself by preventing a procedural reset. A third party also adds credibility if the tenant attacks service. Provide the server with a clean packet: tenant details, unit access notes, and the exact notice version stored in your records.

Build a Court-Ready Notice Workflow

If you are dealing with a difficult tenant, your best move is to shift from improvisation to a repeatable, court-ready system. That means centralizing three things you will need in every contested notice situation: time-stamped tenant communication, clean operational history (maintenance requests, vendor dispatch, resolution notes), and court-ready records (notices, photos, mailing receipts, and proof of service kept together).

Book a demo at shukrentals.com/book-a-demo to see how Shuk's centralized in-app messaging with email and push notifications, maintenance request tracking with photos and documents, and property-organized document storage work together so the next time you need to defend a notice timeline, your records are clean, time-stamped, and exportable rather than scattered across texts, email threads, and camera rolls.

How to Handle Tenant Turnover: A Step-by-Step Checklist to Cut Vacancy Days and Protect Your Property

Tenant turnover is where rental income and property condition are won or lost. One move-out can trigger a chain reaction: unclear notice dates, missed inspection opportunities, deposit disputes, delayed vendors, stale listings, and ultimately extra vacancy days you cannot get back.

Those empty days are not theoretical. Industry reporting breaks down turnover costs as a mix of hard expenses covering cleaning, paint, repairs, lock changes, and flooring, and soft costs especially lost rent, which can represent 35% to 50% of total turnover expense. When you add it up, turnover commonly lands anywhere from $1,000 to $5,000 per move-out depending on unit condition and market, and one analysis pegged average turnover at approximately $3,872 per resident.

The other challenge is time. Even if your make-ready only takes two weeks, the end-to-end vacant-to-leased period can stretch longer when you factor in marketing, showings, screening, and lease signing. Recent analytics showed average vacant days climbing to 34.4 days by the end of 2024. For independent landlords and property managers, that is a painful drag on cash flow, especially when you are juggling maintenance coordination, compliance deadlines, and tenant communications across text threads and spreadsheets.

This playbook is designed to turn turnover into a repeatable system. You will get an end-to-end checklist from move-out notice through move-in onboarding with practical timelines, legal guardrails especially around security deposits, and efficiency tactics that reduce vacancy days while protecting the asset.

Why Turnover Deserves a System, Not Just a To-Do List

Turnover is unavoidable. Preventable chaos is not. Here is what you are protecting with a disciplined process: revenue continuity through minimized vacancy days and lost rent, asset value through consistent standards in cleaning, paint, repairs, and preventive maintenance, and legal compliance especially around deposits, notices, and documentation.

Vacancy time has expanded in many markets. General operational targets often aim for 20 to 30 vacant days for typical properties while market-wide averages can rise above a month. If you wait to market until the unit is empty, start calling vendors after keys are returned, and assemble deposit documentation at the last minute, you are choosing a longer downtime.

This guide walks you through a practical turnover workflow in ten steps matching the real sequence you experience: move-out notifications and confirmation, pre-move-out instructions and scheduling, inspections with photos, security deposit reconciliation and state deadlines, repairs and cleaning and make-ready planning, preventive maintenance upgrades, marketing and re-listing, tenant screening and selection, lease signing and compliance documentation, and move-in onboarding that prevents the next turnover.

Adopt even half of this system and you will reduce friction, create a consistent resident experience, and build a turnover engine that scales from one unit to one hundred without burning you out.

Ten Steps to Reduce Vacancy Days and Protect Your Property

Step 1. Confirm Notice, Lease End Date, and Local Requirements

Start the turnover the moment you receive notice because every day you delay planning becomes vacancy later. Verify the lease end date, the required notice period, and how notice must be delivered whether by email, written letter, or portal. Month-to-month notice is commonly 30 days but can vary by state and circumstance. California can require 30 or 60 days depending on length of tenancy. In Texas, month-to-month is generally tied to one rental period of approximately 30 days.

What to do: Send a written notice-received confirmation that includes the tenant's confirmed move-out date and time, a forwarding address request which is critical for deposit mail in some states, and a timeline of inspections, utilities, and key return.

Use templates and automated reminders so you are not rewriting the same messages every turnover. Centralizing dates in one calendar covering notice received, pre-inspection, move-out, and deposit deadline reduces missed deadlines and he-said-she-said disputes.

Step 2. Send a Pre-Move-Out Instruction Pack

A clean, consistent move-out process protects your unit and your deposit accounting. Within 24 to 48 hours of notice, send a move-out instruction pack covering cleaning expectations for appliances, bathrooms, floors, and trash removal; what counts as normal wear versus tenant-caused damage with defined examples; rules for patching holes, nail removal, and paint touch-ups if you allow tenant repairs; how to return keys, garage openers, and fobs; and utility transfer requirements.

This step reduces your make-ready scope and speeds listing photo readiness. Turnover cost analyses consistently include cleaning, painting, and junk removal as major line items. If your tenant understands standards early, you are more likely to avoid paying for avoidable labor.

A practical 48-hour countdown to include in your message: At T-minus 48 hours, confirm elevator reservation if applicable and final walkthrough appointment. At T-minus 24 hours, remove all belongings, wipe down appliances, and bag trash. On move-out day, take photos, drop keys, and record meter reads if relevant.

Also schedule a pre-move-out walkthrough where allowed. It reduces conflict by aligning on what will be billed before there is a dispute rather than after.

Step 3. Pre-Inspection and Early Scope of Work

If your state and local rules allow, do a pre-move-out inspection one to two weeks before the tenant leaves. The point is not to nitpick. It is to identify safety issues or major repairs that will block leasing, pre-order materials including paint, blinds, filters, and smoke and CO batteries, and get vendor bids scheduled so day one after move-out is productive rather than spent making calls.

Industry estimates place make-ready costs anywhere from $400 to $5,000 or more depending on condition. The earlier you define your scope of work, the more you can keep costs toward the low end.

A standardized inspection rubric with lease-ready minimums: All lights working with covers intact. No active leaks and drains clear. Appliances functional. Doors and locks operating smoothly. Walls with a patch, sand, and paint plan. Floors with a clean, repair, or replace plan.

Create tasks directly from inspection results and assign them to staff or vendors with due dates so nothing exists only in your head.

Step 4. Move-Out Day: Document Condition Like It Is Evidence, Because It Is

Your move-out inspection should be consistent, photo-rich, and time-stamped. Photograph each room from multiple angles, close-ups of damage covering chips, stains, holes, and broken fixtures, appliances inside and out, floors and baseboards, outdoor areas including patio and yard condition, and keys and fobs returned with a count recorded.

This documentation directly supports deposit deductions and protects you if disputes escalate. Many state deposit statutes require an itemized statement of deductions within a specific deadline window often alongside the refund. Photos combined with an inspection checklist make your itemization far easier to justify and far harder to dispute.

Complete the inspection immediately after possession returns when keys are surrendered to avoid ambiguity about post-move damage. If you allow early key return, document the exact surrender date and time in writing.

Also initiate lock changes and re-key immediately after move-out. Lock changes are a standard line item in turnover cost breakdowns and a safety expectation for professional operations.

Step 5. Security Deposit Reconciliation: Meet Deadlines, Itemize Correctly, and Avoid Penalties

Deposit handling is where small process errors can become expensive. Many states require deposit return within 14 to 60 days and several impose strict penalties for late or incorrect handling.

State-specific timelines to know:

California requires return within 21 days with itemized deductions and potential penalties up to two times the deposit for bad-faith retention.

Texas requires refund within 30 days after surrender, often tied to receiving a forwarding address, with bad-faith penalties that can include $100 plus triple damages plus attorney fees.

Florida requires return within 15 days if no deductions are taken. If claiming deductions, written notice must be sent within 30 days and the tenant has 15 days to object. Missing the notice can forfeit the right to withhold.

New York requires return within 14 days with an itemized statement, and missing the deadline can forfeit the right to keep any portion.

Illinois timelines vary based on whether deductions are taken, typically requiring itemization within 30 days and return of the remainder within 45 days.

Best practice workflow: Export the rent ledger and confirm the balance covering rent, fees, utilities, and damages. Separate wear-and-tear from chargeable damage consistently. Attach invoices and receipts when required or when deductions are substantial. Send the itemization and refund via a trackable method. Deadline tracking, templated itemization letters, attachment storage, and recorded delivery reduce legal exposure significantly.

Step 6. Build a 7 to 14 Day Make-Ready Plan With a Day-Zero Vendor Schedule

Treat make-ready like a project plan rather than a to-do list. Your edge comes from scheduling vendors before the unit is empty rather than after move-out.

Example: a three-day repaint schedule that is tight but realistic with proper preparation.

Day zero, the move-out afternoon: patch and sand, clean walls, tape and cover surfaces.

Day one: prime plus first coat with a two-person crew.

Day two: second coat plus trim and door touch-ups.

Day three morning: walkthrough plus punch-list fixes with photos taken the same afternoon.

Pair this with parallel rather than sequential tasks: Schedule the cleaner immediately after paint cures. Have the flooring vendor on standby for spot repairs. Have maintenance handle smoke and CO batteries, HVAC filter, caulk, and fixtures while paint dries.

Because lost rent is often the biggest turnover expense component, shaving even a week off downtime can materially change your annual return on investment.

Step 7. Do Not Skip Preventive Maintenance

Turnover is the best time to do preventive work with minimal resident disruption. Industry maintenance ROI summaries cite findings that preventive maintenance can deliver a 545% return over 25 years and significantly reduce long-run repair costs. Even if your holding period is shorter, the principle holds: preventive maintenance reduces emergency calls, protects your unit, and helps retain the next tenant longer.

High-impact turnover preventive maintenance items: HVAC service plus filter standardization. Water heater inspection covering leaks, the pan, and straps where applicable. Replacement of worn supply lines in bathrooms and kitchens. GFCI testing and outlet and plate replacement. Door weatherstripping to reduce drafts and complaints. Deep cleaning of dryer vents to reduce risk and improve performance.

Create a turnover PM kit per unit type, such as one-bedroom or two-bedroom, with standard parts. Standardization saves time and reduces vendor dependency.

Step 8. Market Early, Keep Listing Visibility Continuous, and Price With Data

Marketing should start while the unit is still occupied if your local rules and tenant privacy considerations allow showings with proper notice. This continuous visibility reduces dead time between make-ready completion and lease signing. General benchmarks suggest aiming for 20 to 30 vacant days, but recent market data showed averages above that, making early marketing a competitive necessity.

What reduces vacancy days: Pre-schedule photography for day one or two after make-ready. Create a listing template with swap fields for rent, deposit, and availability date. Use a showing calendar to batch tours and reduce back-and-forth scheduling. Post a coming-soon notice with an accurate availability date and avoid bait-and-switch situations.

Mini math example: If rent is $2,100 per month, that is approximately $70 per day in gross rent. A make-ready plus leasing delay that extends vacancy from 14 days to 34 days adds approximately 20 days, or approximately $1,400 in gross rent not collected. That is before utilities, yard care, or additional marketing, reinforcing why lost rent dominates turnover costs.

Step 9. Screening: Standardize Criteria, Document Decisions, and Reduce Fair Housing Risk

A rushed screening decision can create the worst kind of savings: a short vacancy followed by late payments, property damage, or another turnover. Build a consistent process covering written screening criteria for income, credit, and rental history; the same application steps for every applicant; and documented adverse action where required in compliance with local rules.

A practical service-level agreement for yourself: Applications reviewed within 24 hours. Verification calls completed within 48 hours. Approval or decline decision communicated within 72 hours.

This matters because turnover already costs thousands per move-out. Avoid compounding the problem with preventable resident churn. Centralizing applications, storing consent forms, tracking communications, and keeping an audit trail is useful if decisions are questioned later.

Step 10. Lease Signing and Move-In Onboarding: Reduce Future Turnover Before Day One

Lease signing is not the finish line. Onboarding is where you prevent the next turnover. Your goals are to set expectations around maintenance reporting, noise, pets, and parking; make rent payment easy and consistent; and capture baseline condition documentation before disputes can arise.

Move-in best practices: Collect funds for first month and deposit as cleared payment before handing keys. Provide a move-in checklist with photo instructions. Confirm how to submit maintenance requests and what constitutes an emergency. Deliver care and cleaning guidance for countertops, floors, and HVAC filters.

Less friction translates into fewer late payments, fewer misunderstandings, and better retention, lowering the turnover frequency that drives those $1,000 to $5,000 move-out costs.

Vacancy Cost Comparison: Reactive vs. Proactive Turnover

Reactive turnover: Market late, vendors scheduled after move-out, no standardized checklist. Approximately 34 vacant days at $70 per day equals approximately $2,380 in gross rent lost.

Proactive turnover: Market early, vendors pre-booked, standardized checklist applied. Approximately 18 vacant days at $70 per day equals approximately $1,260 in gross rent lost.

Difference: Approximately 16 days and approximately $1,120 saved, not including reduced make-ready expenses from early standards communication or reduced legal risk from tracked deposit deadlines.

Tenant Turnover Checklist

A. Notice and planning: Receive written notice and confirm move-out date and time in writing. Verify lease end date and required notice period for your state and local jurisdiction. Request forwarding address for deposit return. Send move-out instruction pack and cleaning standards. Schedule pre-move-out walkthrough if permitted. Pre-book vendors for paint, cleaning, flooring, and handyman with day-zero and day-one slots reserved.

B. Inspections and documentation: Prepare inspection rubric and photo checklist. Conduct move-out inspection immediately after surrender. Take time-stamped photos and video of every room plus close-ups of all damage. Record key and fob count returned and schedule re-key and lock change. Capture meter reads and utility status if applicable.

C. Deposit and compliance: Reconcile ledger covering rent, fees, and utilities balance. Separate wear-and-tear from chargeable damage. Collect vendor invoices and receipts for deductions where required. Send itemized statement and refund within your state deadline with delivery tracked.

D. Make-ready execution: Finalize scope of work and budget covering materials, labor, and contingency. Complete repairs affecting safety and habitability first. Execute paint plan covering patch, prime, and coats. Schedule deep clean after dust-producing work. Replace consumables including filters, bulbs, and batteries and test smoke and CO devices. Complete preventive maintenance covering HVAC, plumbing checks, caulk, and GFCIs. Conduct quality-control walkthrough and punch list.

E. Re-listing and leasing: Update photos and listing description using a template. Set an accurate coming-soon or available date. Schedule showings in batches and follow up with applicants within 24 hours. Apply screening criteria consistently and document decisions. Issue lease, obtain signatures, and collect funds as cleared payment.

F. Move-in onboarding: Provide move-in checklist with photo instructions. Confirm maintenance request process and emergency protocol. Provide rules covering trash, parking, pets, and noise. Deliver keys and fobs and confirm receipt in writing. Schedule optional 30-day check-in to address early issues before they escalate.

Frequently Asked Questions

How long should tenant turnover take from move-out to new move-in?

There is no single national standard because vacancy time includes both make-ready and leasing time. Some operators report make-ready completion in roughly two weeks with leasing under three additional weeks, while broader analytics recorded 34.4 average vacant days by the end of 2024. You cannot control every market factor, but you can control your workflow. Pre-scheduling vendors, marketing early where allowed, and standardizing screening timelines are the most reliable ways to compress downtime toward a 15 to 30 day target range. If your average is consistently above a month, start by tracking where time is actually spent: waiting on bids, waiting on cleaners, slow applicant follow-up, or delayed listing photos.

What can I legally deduct from a security deposit?

Generally, and state rules vary significantly, you can deduct for unpaid rent and fees and for tenant-caused damages beyond normal wear and tear, supported by an itemized statement and documentation. New York requires return and itemization within 14 days. Florida distinguishes between no-deduction returns within 15 days and deduction claims requiring notice within 30 days. California requires return within 21 days and may require receipts depending on deduction amount. Because penalties can include forfeiture of withholding rights or statutory damages, treat deposit handling like compliance work with consistent inspection photos, clear invoices, and deadline tracking.

Should I renovate during turnover or just do minimum make-ready?

It depends on rent upside and your holding strategy, but do not confuse minimum make-ready with no preventive maintenance. Lost rent can represent 35% to 50% of total turnover cost, so prolonged renovations can erase returns if they extend vacancy too far. A balanced approach is lease-ready now plus preventive maintenance always. Use turnover for fast, high-impact work including paint refresh, fixture swaps, and hardware standardization alongside preventive items that reduce future emergencies. If you are considering a bigger upgrade, run the math: added rent times expected tenancy length minus renovation cost minus additional vacancy days.

How do I reduce turnover time if I only manage a few units and do not have staff?

Your advantage is agility if you build a repeatable system. Start by templating everything: notice confirmation, move-out instructions, inspection rubric, deposit itemization letter, listing description, and screening criteria. Next, pre-build a vendor bench covering painter, cleaner, and handyman and keep turn slots reserved each month. Turnover costs commonly land in the $1,000 to $5,000 range and average vacancy days can exceed a month, so even a small reduction in downtime is meaningful cash flow. If you are overwhelmed, an all-in-one management platform is often the simplest operational upgrade: one place for leasing, screening, e-signatures, payments, maintenance, and document storage.

If tenant turnover feels stressful, it is usually not because you do not know what to do. It is because the process is spread across too many tools, too many messages, and too many mental reminders. The checklist above works best when it is operationalized so tasks generate automatically when notice is received, deposit deadlines are tracked by state, vendors and inspections are scheduled from a single calendar, listings publish quickly, applications flow into one screening pipeline, and all documentation is stored in one place.

Book a demo to see how Shuk's turnover tools work, including task templates, automated reminders, centralized documents, leasing and screening pipeline, and move-in onboarding workflows, so your next turnover is the last one you manage through scattered notes and last-minute scrambling.

5 Steps to Take Back Control of Your Property Management

Losing control of your rental portfolio rarely announces itself. It shows up quietly: a missing receipt at tax time, a tenant waiting three weeks for a repair update, or a property manager who says they handled it but cannot produce the paper trail. And if you are new to landlording, maybe you inherited a property or bought your first rental, the learning curve gets steeper as you grow from one unit to five, then ten.

The stakes are real. Nearly 46% of U.S. rental units sit in one to four-unit properties, and individual investors own the vast majority of those homes, the exact group most likely to be running lean on back-office support. When your systems are loose, costs climb through vacancy drag, maintenance surprises, and legal exposure, and you end up reacting instead of planning.

This guide walks you through five practical steps to regain control, whether you are transitioning away from a third-party manager or tightening up your self-management operation. You will leave with concrete examples, compliance reminders tied to real statutes, and a plug-and-play checklist you can start using this week.

What Control Actually Looks Like for Small Landlords

Control does not mean doing everything by hand. It means you can answer key questions quickly and confidently.

Operationally: what is the status of every open maintenance item, who is responsible, and what is the timeline? Financially: what did you actually net last month per unit after repairs, utilities, and fees? From a compliance standpoint: are your leases, notices, and deposits aligned with your state's current rules? From a tenant experience standpoint: do tenants know how to reach you, what to expect, and how issues get resolved?